During 2018 the Fed paid out the incredible sum of $43.1 billion to pretend that it was fixing the overnight funds rate.

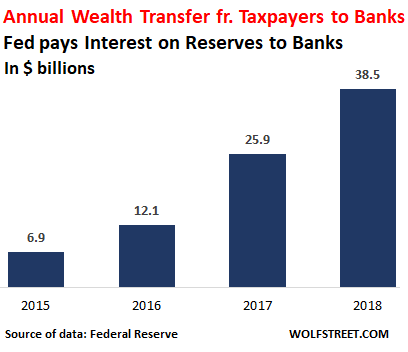

That’s right. Banks got $38.5 billion in IOER payments (interest on excess reserves) for keeping roughly $1.5 trillion of excess reserves on deposit with the Fed. For the last four years together, the IOER hand-out totaled more than $83 billion, as shown in the chart below.

At the same time, other Wall Street nonbank financiers picked up a nifty $4.6 billion for lending cash to the Fed—loans which were collateralized by UST securities from the Fed’s massive portfolio (reverse repo program or “ON RRP”).

Surely, there is no more ludicrous case of taking “coals to New Castle” than these maneuvers—even if the Fed heads have gussied them up with obfuscatory acronyms.

To wit, possessed with its very own printing press, why in the world would the Fed ever borrow a single dime of cash via ON RRP? The very idea of it is just plain nuts.

Worse still, why would it bribe banks with $38.5 billion of IOER payments so that they would not lend money to private borrowers at lower rates than its target range for the fed funds sector?

Yes, these whack jobs actually threw $38.5 billion of good money at the US banking system last year so that it wouldn’t lend too cheaply!

But that’s not the half of it!

All of this nonsense was undertaken in order to insure that fed funds rates stayed exactly within the Fed’s prescribed 25 basis point range. Yet why does it even bother trying to peg the funds rate when the funds market is essentially deader than a doornail, and has been ever since Bernanke killed it in the fall of 2008 with his massive money pumping operation and hair-brained scheme to pay interest on excess reserves?

As shown below, during the pre-crisis period in 2007, volume in the Fed funds market averaged about $200 billion, which figure comprised about 2.4% of total banking system liabilities of $8.3 trillion.

But after Bernanke turned on the spigots and flooded the banking system with excess reserves, the Fed funds market virtually disappeared, and currently averages about $70 billion of buy-sell volume or just 0.6% of the current $13.3 trillion of total bank liabilities.

Indeed, even as the Fed was purportedly raising interest rates over 2017-2018, there was no sign of tightening in the Fed funds market—at least as measured by volume. During that period, average volumes generally fell sharply, almost to the vanishing point.

Moreover, even the tiny volumes which remained in the fed funds arena amount to essentially a hothouse simulacrum of a market. That is, more than 90% of the funds supplied are advanced by government guaranteed agencies (GSEs) called Federal Home Loan Banks (FHLB).