Who would have guessed it—even 15 years ago? And that’s to say nothing of the salad days of American prosperity six decades back when capitalism flourished and the Fed exercised a Lite Touch on the monetary dials.

We are referring, of course, to the Donald latest tweet revealing that he—ostensibly a Republican president—-just meet with the Federal Reserve Chairman to discuss among other things, negative interest rates, more easing and low inflation.

Just finished a very good & cordial meeting at the White House with Jay Powell of the Federal Reserve. Everything was discussed including interest rates, negative interest, low inflation, easing, Dollar strength & its effect on manufacturing, trade with China, E.U. & others, etc.

Regardless of how Powell bobbed and weaved in the face of this blithering POTUS nonsense, the mere fact that such monetary crackpottery was discussed in the White House (East Wing residence, at that!) tells you all you need to know about today’s financial madness.

To wit, not only have decades of Keynesian central banking blatantly falsified the prices of financial assets— it has also deeply falsified and corrupted the financial narrative itself. The very propositions implicit in the Donald’s tweet that we need easier money because inflation is too low, the dollar’s too strong and there’s negative interest rates abroad are demonstrably ludicrous.

Yet they are considered valid by most of Washington and much of Wall Street—and at least debatable by even mainstream skeptics who think the Donald over-states the matter.

In truth, however, what is relevant to the proper functioning of the mainspring of the entire financial market is the relationship between inflation and the money market rate of interest. In any rational, stable and sustainable financial system the spread of money cost over inflation must always be positive, and vary wider or narrower over time based on the supply and demand for funds.

Yet the Fed funds rate crossed under the running inflation rate way back in March 2008 when it stood at 2.60% versus the 16% trimmed mean CPI, which posted at 2.95% on a year-over-year basis. At that point, the real money market rate computed to negative 35 basis points, and remained in negative territory–sometimes by 200 basis points or more—for the next 130 months running.

There is no precedent for anything like this in all of financial history–even during the Great Depression, as shown below. That’s because negative real interest rates on a sustained basis are completely impossible on the free market where use of money has an inherent time value, and are only possible under conditions of extreme central bank financial repression of a virulence that wasn’t even imaginable before the 2008 financial crisis.

So the last decade has been an assault on financial law itself—-to say nothing of the savers and fixed income retirees who have been financially brutalized and expropriated by this toxic regime of negative cost money.

Indeed, it wasn’t until January 2019 that a positive real money market spread peeked out from the shadows of the Fed’s long night of financial repression. At that point, the money market benchmark rate (Fed funds) returned to 2.40%, thereby reflecting the grand sum of 21 basis points of positive real yield compared to the running inflation rate of 2.19%.

Needless to say, under the combined onslaught of the crybabies and entitled gamblers of Wall Street and the ignorant bully in the Oval Office, that interval of positive money market spreads lasted just seven months. As is evident in the chart, the spread turned negative again by 11 basis points in August after the Fed’s rate cut capitulation at its July meeting, and its been off to the races ever since.

Today, the Fed funds rate stands at 1.55% versus an October year-over-year inflation reading of 2.35%.

That’s right. We are back to negative 80 basis points on the real cost of money, yet we have a lunatic in the Oval Office who wants the Fed to drive the spread even deeper into negative territory, thereby further defying every traditional canon of sound money—to say nothing of economic rationality itself.

After all, the chart below already shows that during the last 140 months, there have been only 7 months in which the Fed funds rate was above the broad inflation rate, as consistently measured by the 16% trimmed mean CPI.

As can be demonstrated six ways to Sunday, this aberrant condition has done nothing for main street because the problem of the latter since 2008 has been Peak Debt, not high interest rates.

To the contrary, negative real money market rates are simply the mother’s milk of carry trade speculation. They generate financial asset inflation and all the distortions and economic infirmities which flow from it—but not any progress at all toward the Fed’s purported mandates of full employment and 2.00% goods and services inflation.

Indeed, the truly aberrant nature of the past 11 years is dramatically evident in the same chart for the decade of the 1930s, albeit with the commercial paper rate serving as the proxy for the short-term money market rate. Yet notwithstanding the virtual collapse of private borrowing during much of the Great Depression decade, nothing like the pattern since March 2008 is evident.

In fact, the money market rate (blue line) was positive in real terms during 86 months of the 125 month period encompassed by the chart or 69% of the time. That’s a far cry from the 5% of months in which there has been positive real carry since March 2008.

Something else is evident in the 2008-2019 central bank fostered aberration in the money market, as well. Namely, the claim that the Fed has fallen consistently behind its sacred 2.00% inflation target—thereby justifying severe and relentless financial repression—just isn’t true.

The chart below covers the 29 years since 1990. The general price level as measured by the 16% trimmed-mean CPI has risen by 94% or an average of 2.3% per year. We’d not call that “low inflation” because a dollar saved by a young worker in 1990 will buy just $0.53 worth of goods and services in his retirement today.

Nor are we picking the longest measuring stick around—even if conceptually the 16% trimmed mean CPI is nothing more than a short-and-medium term smoothing device to index the underlying basket of goods and services.

Indeed, the other inflation index shown in the chart is the Fed preferred PCE deflator, and it too has risen mightily since 1990 and now stands 70% higher. That amounts to 1.9% annual inflation and $0.59 of purchasing power today for the dollar saved in 1990.

To be sure, the PCE deflator is not really a inflation index which measures the purchasing power of money over time. Instead, its a statistical device used by the government data mills to deflate GDP and its components based on the changing composition of purchases—including the “deflation” which results during hard times when consumers substitute spam and carp for steak and lobster.

Still if you average the two indices shown below over the last three decades you get 2.1% annual inflation. That’s close enough to 2.00% to call it mission accomplished—even if the mission is profoundly inequitable and counter-productive.

That is, either way savers and retirees have been shafted without any proof at all that the Fed’s mindless pursuit of easier money results in more inflation and more growth.

Yet the ritual incantation doesn’t stop, as evidenced by the Fed’s claim it can ease to please Wall Street because inflation is below target—to say nothing of the Donald’s relentless refrain of the low-flation chorus.

The ostensible reason, however, is about as lame as it gets. To wit, during the 21-years between 1990 and Q4 2011, the trimmed mean-CPI rose by 2.43% per annum and the PCE deflator by 2.05% per annum. Mission more than accomplished, therefore.

By contrast, since inflation-targeting was officially adopted by the Fed in January 2012, the 16% trimmed mean CPI has continued to post at 1.94% per annum or about as close as you please to target, while the PCE deflator has weakened to 1.38% per annum.

But the latter is not because suddenly American capitalism caught some mysterious low-flatation disease.

It’s because the PCE deflator substantially underprices medical inflation, and has been further pulled-down by commodity and industrial goods deflation owing to a global supply/demand imbalances originating in the Red Ponzi and its supply chain—a beneficent condition for American consumers that the Fed should not attempt to correct and can’t anyway.

And that gets us to the broader issue of the Fed’s impotence when it comes to goosing main street growth and jobs—the ostensible purpose behind Trump’s relentless hectoring of Jay Powell and his pusillanimous posse of money printers.

It is now evident that the industrial economy is sliding into recession—after a record 125 months of stop-and-go expansion. Since December 2018, industrial production, real business CapEx and total private construction spending have all been flat-lining—notwithstanding the fact that the Fed and other central banks around the world have pivoted to a so-called “easing” mode.

But after decades of easing and $22 trillion of central bank balance sheet expansion since the late 1990s, the real economy is now immune to marginally lower interest rates or an upturn in central bank asset purchases.

These maneuvers accomplish one thing alone: That is, they cause a further inflation of financial assets— as the casino’s stock average have been recording—which only fuels more C-suite financial engineering and destructive speculation in the money and capital markets.

But proof of the pudding lies in the chart two charts below. The first one shows that US manufacturing output has again entered serious negative territory. The post-tax cut sugar high is over and done.

The second one shows that the above collapse of mfg. shipments has nothing to do with the Fed’s short-term policy rate and balance sheet machinations. Basically, the global commodity cycle—-crystalized in the trend of crude oil prices—explains the start-and-stop undulations of the manufacturing sector and the overall economy which on the margin it drives.

You really do not get much more close coupling than shown by the slight lag of the purple line (U.S. mfg. output) with the brown line (the Brent crude oil price).

For instance, when Brent Crude hit bottom in January 2015 at 56% below its prior year level, US manufacturing output bottomed a few months later in December 2015 down 7.3% versus prior year.

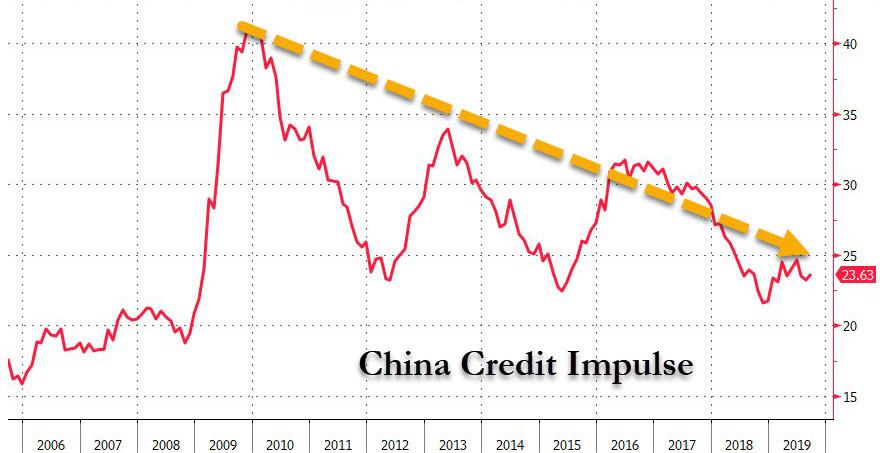

Then in response to a huge credit impulse from China in the run-up to Mr. Xi’s coronation as ruler for life in October 2017, the Brent oil price peaked in early 2018 up by 65%, while U. S. manufacturing output surged to a 8.4% year-over-year gain by July.

Finally, by December 2018, the Brent crude price had drastically rolled-over and was down by 24% from prior year. With a few months lag, US manufacturing output has again taken the same dive lower.

Needless to say, this time there is no Red Ponzi coming to the rescue. The Red Ponzi is driven by credit-fueled fixed asset investment growth, but that has now dropped below 5%—-the lowest year over year rate since China elected the Deng Xiaoping route in the early 1990s.

That is, the proposition that Communist Party power flows from the end of a central bank printing press rather than Mao’s claim it came from the barrel of a gun.

But the printing press route to socialism has now reached its sell-by date, as well. That means, ironically, Beijing is between a true rock and a hard place.

If they attempt another massive credit expansion, Yuan’s exchange rate will collapse in the face of relentless capital flight—even as it will force the Donald to up the ante in his China-destabilizing Tariff assault. And if they don’t open the credit spigot, the great Red Ponzi will slide ever faster into the final debt-boom fueled crack-up.

Either way, the Red Ponzi will not come ridding to the recue this time—meaning that the sinking US industrial economy is heading down for the count.

But, shhhh, don’t tell the Donald!