The Donald’s being taken to the cleaners by his top staffers again, but in his blissful ignorance he is actually urging them on. We are talking about the Fake China Trade Deal coming down the pike and the comedy of errors and contradictions it will entail.

The heart of the matter is that Trump cares about the real problem, which is America’s $400 billion trade deficit with China (2017), and his advisors don’t. The so-called free traders have their heads buried in the sands of abstract theory and the protectionists have their hands out to the K-street lobbies and corporate crybabies for whom they are carrying water.

So as a starting point to untangle this latest Trumpian Gong Show, let us recall the shocking magnitude of the US/China trade gap and the manner in which is has metastasized. That is, it’s the bastard step-child of bad money—- not bad trade deals, nefarious doings of the Chinese state and most especially not the unseen hand of the free market.

To wit, between 1993 and 2017 US imports from China grew from $20 billion to $530 billion (dark blue bars). But nothing grows by 27X in barely two decades in the natural order of markets, and not in a context in which the US export side of the equation stands at a tiny 25% of imports.

That is to say, there can be large trade imbalances between countries owing to comparative advantage and specialization, as well as to mercantilist trade practices.

But imbalances this freakishly large and persistent cannot be attributed to either economics or protectionism. Instead, they are a function of money gone bad during the Fed-driven global central banking print-a-thon of the last several decades.

The Freakish Evolution Of The US/China Trade Imbalance

Of course, the Donald doesn’t get the bad money thing at all. Perhaps it has never occurred to him that the decades of ultra-low interest rates on which his leveraged real estate empire was built were the fruit of the Fed’s insidious campaign to stimulate more domestic inflation on the misbegotten theory that rising prices are a growth tonic.

Even in ordinary circumstances, central bank stimulation of commodity and consumer price inflation can only wreck havoc with prosperity by fostering excessive debt, speculation, inefficiency and malinvestment—even as it capriciously transfers economic resources from savers and retirees to borrowers and leveraged gamblers (e.g. in real estate!).

But under a circumstances like the early 1990s it was downright perverse. That’s because when upwards of a billion workers, who had been sequestered from world markets by the Soviet “iron curtain” and the Chinese “bamboo curtain”, were suddenly liberated to participate in global commerce by Yeltsin and Deng, it caused an unprecedented deflationary shock.

Essentially, the labor and supply cost curves of the world economy were re-set to a drastically lower point than had been built-up over the decades since WWII by the monopoly industrial unions of the US and Western Europe and the mildly pro-inflation policies of their central banks.

That meant, in turn, that the inflated price/cost/wage level in the US needed to be systematically deflated in order to maintain competitive equilibrium. And that would have actually happened under an honest free market and a regime of sound money.

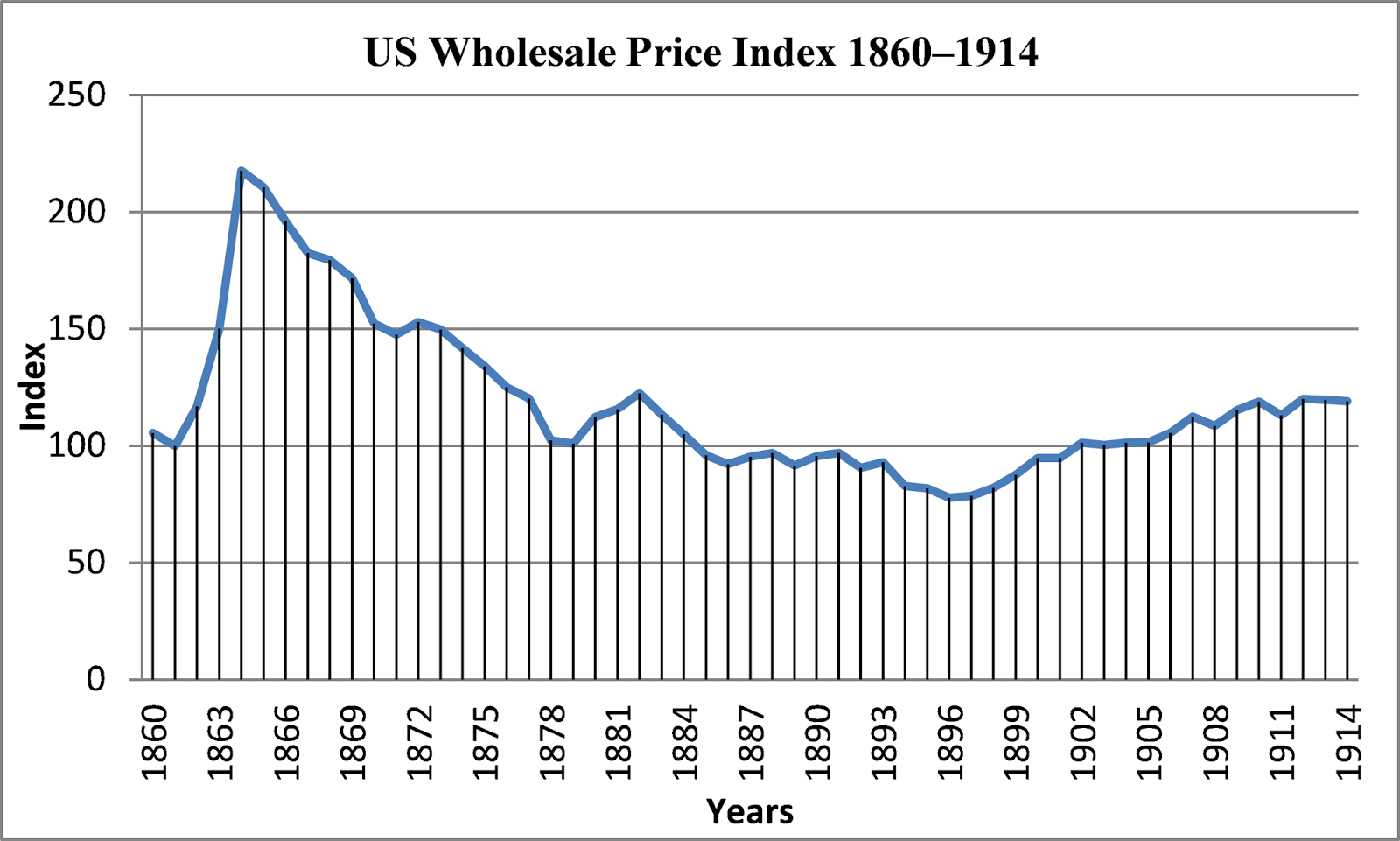

Indeed, there is almost a perfect parallel in the second half of the 19th century when the US experienced a massive inflow of essentially peasant labor from Ireland, Italy, Germany, Poland and the rest of old Europe. Shortly after the Civil War, in fact, the US population stood at 48 million (1870), but during the next 40 years more than 35 million immigrant workers and their families came through Ellis Island.

That inflow of cheap labor kept wage levels down and permitted wholesale prices in the US to fall for several decades. In essence, the Civil War induced inflation of the 1860s stemming from Lincoln’s greenback money was the equivalent of the post-WWII price level inflation in the US.

But after the early 1870s, the US went back on the gold standard, meaning that even as growth boomed under the railroad and industrialization revolutions of the period, the Civil War inflation was liquidated and the price level ended-up close to where it started before Lincoln turned on the literal greenback printing press to finance it.

The irony, of course, is that the inflow of cheap labor into world commerce that had been sequestered in the statist poverty of the communist world occurred conterminously with Alan Greenspan’s baleful 19-year term as head of the Fed and Maestro of the world’s financial system.

As it had happened, Ronald Reagan was persuaded to fire hard-money man Paul Volcker by the White House pols and replace him with Greenspan. That’s because he was under the impression that the latter was actually a gold standard advocate, as was the Gipper in private moments when he was not being scripted by the Wall Street operatives and Keynesian economists which populated his Administration.

In any event, after famously bringing Ayn Rand to his swearing in ceremony as CEA Chairman during the Ford Administration, Greenspan soon learned that sound money and Republican politics had parted ways at Camp David in August 1971; and that the updated version of the gold standard consisted of the Monetary Eunuchs at the Fed, which Uncle Milton Friedman had decreed would henceforth safeguard the value and integrity of the nation’s money.

That is, sitting on the FOMC they would deftly guided the growth of M1 along a stable and disciplined path that trended toward 3% per year under normal circumstances, representing the good professor’s belief that potential real GDP could grow at 3% annually and consumer level inflation should wash-out to zero over time.

Without saying it explicitly, Friedman held out that the FOMC’s apolitical, non-ideological Monetary Eunuchs would function as a gold standard surrogate. So doing, they would provide all the advantages of the latter, while possessing the human flexibility to recognize that under extraordinary and exigent circumstances—such as the early 1930s—the rigid discipline of the gold standard could be suspended in the name of crisis-fighting.

Needless to say, Friedman was wrong about the gold standard cause of the Great Depression and Alan Greenspan was no apolitical eunuch. He was actually possessed by an intense lust for power and praise and an immense capacity for self-serving rationalization and casuistry.

Indeed, many years after he left office we heard him say to a group of sound money people that he had been with us all along. Under his watch, the Fed had actually attempted to function as a surrogate gold standard!

In fact, the only abnormal and exigent circumstance that existed after 1991—when the Soviet Union disappeared and the captive nations and republics were liberated in the West and Mr. Deng flung-open the export factories and Beijing’s printing presses in the east—-was virtually identical to that which existed at the time of gold standard resumption in 1873.

Namely, a lot of accumulated inflation needed to be wrung out of US price and wage levels at best, and at least not added to as a more practical second best.

But here is the truth of the matter. To insure that he did not get Volcker’d by the very political assassins who had done in Tall Paul—that is, the Jim Baker wing of the Bush coterie—-Greenspan deftly invented his own form of surrogate for the actual gold standard deflation that was urgently needed.

He called it “disinflation”, which was a disingenuous and rubbery concept that essentially meant whatever rate of CPI gain that resulted from running the Fed printing presses overtime—so long as it was reasonably lower than the extreme inflation of the 1970s.

Accordingly, the path was set for a cumulative gain in the domestic price level that under the circumstances would have been inconceivable under a regime of sound money. Between 1992 and the end of his term in 2006, the CPI rose by 44%; and it was levitated ever higher by his inflation targeting successors.

Bernanke got the domestic price level to a point 68% higher than its 1992 starting point by the time he left office; and the two Janets (Yellen and Powell) in succession have taken the CPI to 83% of where it stood when the flood of cheap labor began pouring into the global economy after 1991.

Needless to say, the contrast between the chart below and the one above is all you need to know in order to grasp the profound “bad money” roots of the America’s trade account collapse and the hollowing out of its productive economy and goods jobs which has resulted therefrom.

So the Maestro got re-upped by the Baker-Bush folks in 1991 and their bipartisan fellow-travelers in the Clinton and Bush II administrations thereafter. But the Fed’s pro-inflation policies have been an exercise in sheer folly and are at the very root of the contretemps now under way in the form of the Donald’s misbegotten Trade War with China and others.

To wit, fully loaded manufacturing wage costs (including payroll taxes, health insurance, pensions and other fringes) were about $12 per hour back then (1989), but exceed $30 per hour now.

So even though Chinese manufacturing wages in US dollar equivalents have risen from under $1 per hour to around $5 per hour during the same 30 year period, the absolute gap has widened: From $10 per hour in the early 1990s to $25 or more today.

It is the systematic and persistent widening of the dollar cost gap over the last three decades which accounts for the massive US trade deficit with China, not the WTO, cheating Chicoms or dumb trade deals.

And that’s true even after you factor in higher productivity in US factories, an advantage which is rapidly diminishing as China automates and robotizes its factories, and also the incremental costs of a 5,000 mile supply chain, which includes sourcing, transportation, insurance, the carry costs of buffer stocks etc.

Needless to say, all of that Fed sponsored inflation of domestic wages did exactly nothing for American workers. Since 1979 when the US trade balance plunged into deep, permanent deficits from which it never recovered, in fact, average hourly wages of production workers have risen 275% in nominal terms.

Yet inflation-adjusted wages of full-time workers are actually 5% below where they were 40 years ago.

It goes without saying that under a regime of sound money, the above depicted gap between ever rising nominal earnings and stagnant real wages would never have happened. That’s because faced with ballooning trade deficits after the later 1980s, when the wage gap was $12 versus $1 per hour, the US price level would have deflated owing to the drain on gold or other FX reserves, which, in turn, would have triggered credit contraction and downward adjustment of domestic prices, costs and wages.

Accordingly, the last 30 years would have seen a narrowing of the US/China wage gap, not a destructive explosion to the more than $25 per hour level which prevails at present.

The deflationary path not taken, therefore, explains how US imports from China grew from $20 billion in 1993 to $530 billion at present. But rather than go to the source of the problem in the Eccles Building, the Donald is being bamboozled by the swamp creatures of K-Street.

As we will detail in Part 2, that amounts to embracing a made-in-Washington Trade Nanny solution that will not remotely close the gap, but will open-up an unending Managed Trade War with China and countless others.