The daredevils left in the casino keep nibbling at the dips, but the so-called “incoming data” keeps reminding us that they are on a fool’s errand.

What we are saying is that the overall financial and economic landscape is exactly the opposite of the “greatest economy ever” about which the Donald so cluelessly boasts. Neither the ballyhooed U-3 unemployment rate at 3.7% nor the Dow at 27,300 measure sustainable success; they are actually flukish artifacts of the monetary and economic rot down below.

When it comes to the core fundamentals, in fact, there has never before been end-of-cycle conditions this bad. That is to say, global debt markets are busted and allocating massive amounts of capital to a desperate but growth-retarding search for yield; equities are egregiously overvalued and hanging from a fragile skyhook; corporate profits are flatlining, not soaring as claimed; and the debt encumbered main street economy is running out of gas after a 121 month business expansion that has been so weak that it hardly deserves to be called a recovery.

We will address all of these conditions in this multi-part series, but start with the latter point—where today another case in point was posted.

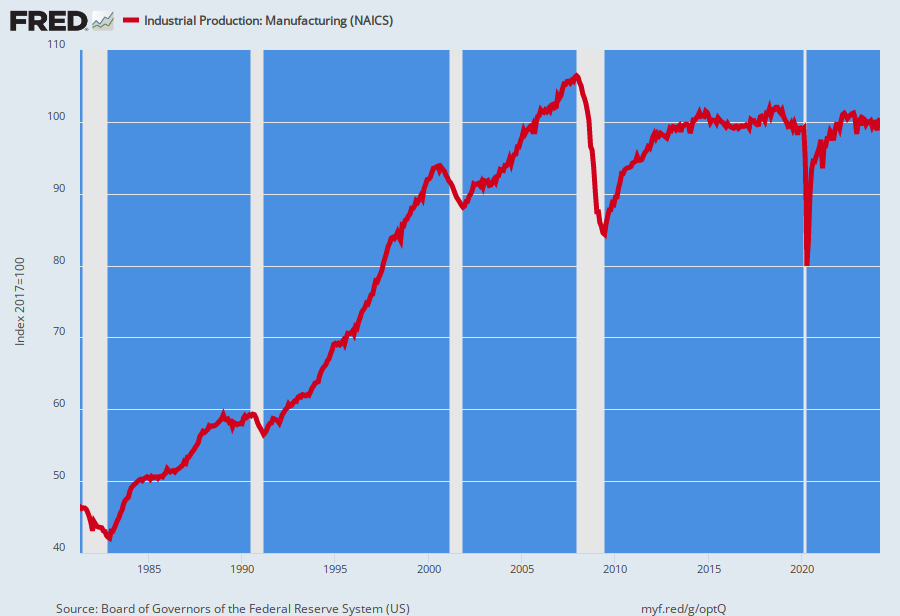

While the talking heads gummed about a slight uptick in the June industrial production number for manufacturing output, the truth is you can’t see it at all on a chart which has any time distance to it. In fact, when the June number is assessed within its cyclical context, it was downright punk.

In the near-term, the 106.3 index reading for June was still below the sugar high of 107.5 reached last December in response to the Trumpite/GOP credit card-based business tax cuts. After six months of retreat since then, the hook lower in the far right hand panel looks suspiciously like the those evident before the 2008 and 2001 recessions, respectively.

More importantly, the June print was actually 1.6% below the level posted at the pre-crisis peak way back in December 2007. In fact, the 12-year growth rate across this entire business cycle now stands at -0.20% per annum.

Needless to say, that’s about as sharp a break from prior history as you can find. By contrast, the first three panels in the graph below show real economic recoveries of the historic kind.

Thus, during the 1981-1990 Reagan Recovery cycle, the growth rate of manufacturing output on a peak-to-peak basis was 2.8% per annum; growth during the 10-year 1990s cycle (June 1990-February 2001) posted at 4.5% per year; and the 2001-2007 cycle registered an annual gain of 2.3%.

In short, a healthy economy can’t survive on Pilates studios, nursing homes and day care centers alone. It needs to make stuff—even if it specializes in product lines of comparative advantage.

But when it rolls into the next recession from a base which is actually lower than the prior peak, it signals a fundamental deterioration in competitive position and capacity for healthy future expansion.

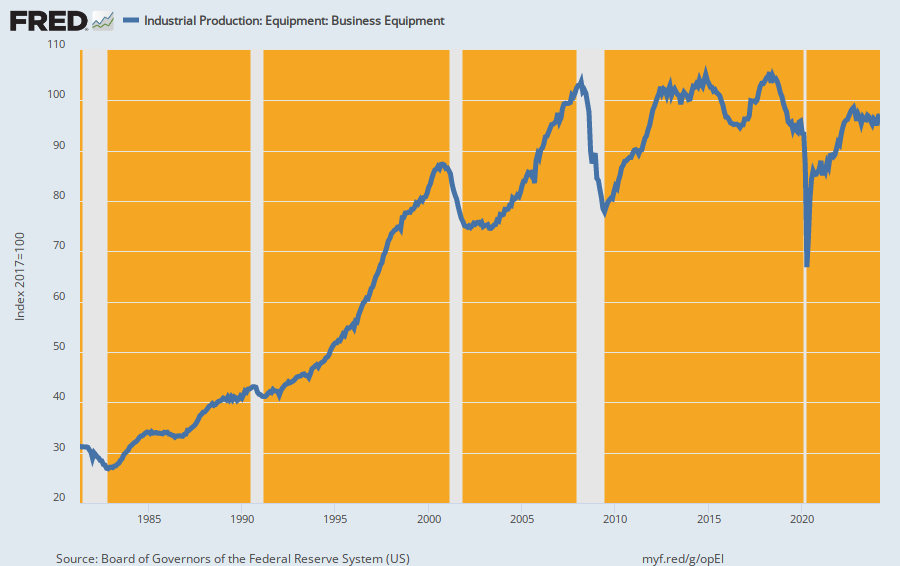

When the manufacturing aggregates are decomposed, the story become even more striking. In a world teeming with low cost labor, the one thing the US economy needs is higher investment in business equipment, thereby providing more tools per worker.

In fact, however, production of business equipment has flat-lined during the past 11 year cycle—again marking a sharp departure from earlier business expansions. Thus, the annualized gain during the 1980s cycle was 3.6%, which then surged to 6.9% on a peak-to-peak basis between June 1990 and February 2001.

Even the tepid production rate during the 2001-2007 cycle registered positive gains of 2.6% per annum. By contrast, the production index for June posted at 102.1 or exactly the same level as the 102.1 recorded back in December 2007 and well less than the 103.9 posted in November 2014.

Yes, there has been a substantial increase in business equipment imports since the pre-crisis peak, but that begs the question. Namely, why should the US economy be incapable of competing in the capital intensive production of business equipment in the global economy?

When it comes to the production of consumer goods, of course, there has been outright retrogression since the December 2007 pre-crisis peak.

After rising nearly continuously at a 2.1% annual rate across three business cycles between 1981 and 2007, output of consumer goods production dropped by 14% during the Great Recession, and essentially never really recovered.

Output in June 2019 was still 7.2% below the pre-crisis peak level and at a level first reached way back in November 1999.

As we will develop further in Part 2, the only real expansions in the US main street economy since the fall of 2007 have been in government supported areas such as health care and education and energy production owing to the massive shale boom funded with cheap debt.

But that, too, does not represent solid organic growth because it has been financed by a CapEx spree which has produced negative economic returns.