The estimable David Rosenberg summed it up well in his morning missive today:

“We are on the precipice of an earnings recession and the market is soaring. Is there a chapter in the classic Security Analysis by Graham & Dodd that I missed on trade talks and border wall funding?

Well, yes, there is a missing chapter. We are referring to the theory of a long line of academic scribblers from Milton Friedman to Ben Bernanke. They essentially hold that the free market is a wonderful thing—-except, except when it comes to Wall Street and matters of money and credit.

Purportedly, such financial prices as the money market interest rate, the shape and level of the bond yield curve and even the capitalization rates for equities and risk assets are too important to be left to the blind price discovery and market clearing processes of supply and demand.

For all of these crucial money and capital markets inputs to capitalist prosperity you need, ironically, a monetary politburo.

That is, 12 especially astute members of the FOMC who can gaze upon the infinite complexities, swirling cross-currents and manifold undulations of a $20 trillion economy; and from that vast information upload, divine the precise interest rates and financial asset prices which will optimize growth and inflation at any point in time, and which will always and everywhere ward off recessions and underperformance arising from external shocks and other untoward acts of god and man.

Of course, Professor Milton Friedman and other forbears of contemporary Keynesian central banking never put it that bluntly, hiding behind a quantity theory of money and obsolete view of bank-based credit, instead.

As most economics majors would recall, Uncle Milton said the job of the Fed was to control the quantity of bank reserves (at a steady pace of @3% growth), which with a lag would drive the quantity of money (M1) and the level of GDP.

Standing between bank reserves and M1, of course, there was the matter of the money multiplier; and juxtaposed between M1 and GDP there was also the critical link known as the velocity of money turnover.

Friedman never did say why these crucial lynch pins in the transmission belt of bank reserves, money and GDP would stay constant over time and across different banking technologies and regulatory regimes; or that if they were changing, how you would estimate and quantify the revised ratios.

He just said there were lags and leads, and that you needed to read his regular Newsweek column for an update at any particular moment.

Alas, since Friedman departed for the economists’ hereafter in 2006, we have had no updates as to the money multipliers and velocities of money.

But no matter. Regulating the quantity of money was always just a backdoor route to regulating its price; and in today’s digital world, bank money doesn’t matter all that much, and bank reserves even less.

Obviously, in the ancient world that Friedman had studied for a lifetime, a deficiency of bank reserves tended to cause stringency of money and high rates of interest; and a surfeit of reserves, just the opposite.

So Friedman was ultimately a financial asset price-pegger, whether the great free market thinker wanted to acknowledge it or not. That is, by getting the quantity of money (M1) just right, the monetary politburo FOMC would allegedly get the prices of interest and financial assets just right, too.

Of course, buried in that monetarist catechism was Keynesian statist economics pure and simple. That’s because on a true free market, no agency of the state regulates interest rates or financial asset prices or their precursors such as levels of credit, money or commercial bank reserves.

All of these are unplanned and unmanaged outcomes on the free market where prices for goods, services and financial assets are discovered by private actors, not pegged by state authorities.

Accordingly, there is no knowable “right price” for overnight money market loans (e.g. Fed funds), 10-year Treasury yields or the S&P 500 index—to say nothing of ludicrous central banker inventions like r-star or the so-called natural rate of interest.

To the contrary, wealth and welfare are optimized when thru trial and error and auction the free market finds the right level for this myriad of financial asset prices based on the ever changing conditions, circumstances, technologies, consumer preferences, fads and all the other dimensions of human action.

Needless to say, that proposition cuts to the heart of the matter. Keynesian central banking, including Friedman’s monetarist branch, presumes that free market price discovery in the financial system is inherently flawed and will led to sub-par growth, recessions, depressions and worse.

It’s as if capitalism has a death wish, which only an activist, asset price targeting central bank can expunge and thereby keep the main street economy on the straight and narrow path to the nirvana of Full Employment.

To be sure, back in Friedman’s time it wasn’t so easy to see that he was a statist monetary central planner. That’s because bank money seemed generally linked to credit and GDP and banking technology and regulation adhered to the old-fashioned (and not erroneous) idea that demand deposits in a fractional reserve banking system needed to be backed by some reasonable level of liquid cash reserves—lest the banking system become too vulnerable to a run.

Needless to say, owing to changes in banking regulation, product innovations such as sweep accounts and digitized banking technology, the importance of checkable deposits and required reserves backing them has faded into near oblivion.

Since 1975, when the old world of banking began its drastic evolution, in fact, total US bank liabilities (blue line) are up by 19.0X, checkable deposits (brown line) by just 9.8X, and required bank reserves (purple line) have risen by only 5.6X.

Stated differently, required bank reserves prior to 1975 amounted to 4-5% of total liabilities, but currently total only $190 billion. That’s just 1.3% of bank liabilities and 0.95% of GDP—a rounding error.

So by the time that Greenspan got his printing presses cranked up in the late 1980s and 1990s, the importance of regulator required bank reserves were going the way of the dodo bird. So instead of perpetuating the Friedmanite fiction that the central bank was regulating the quantity of bank reserves and money, the Greenspan Fed just got right to the price term and the business of overt monetary central planning.

That is, pegging interest rates, the yield curve and risk asset prices (via the infamous Greenspan Put) in a manner explicitly designed to manage the macro-economy as represented by employment, inflation, GDP and it major components such as consumption spending, business CapEx, retail sales, auto production and housing starts.

Stated differently, Janet Yellen and Jay Powell are simply the legatees of Milton Friedman with the monetarist bark peeled off.

Needless to say, the giant problem with naked monetarism cum Keynesian monetary central planning is that in targeting, pegging and falsifying financial asset prices, the FOMC eventually became a hostage of Wall Street. So doing, it steadily lost sight of any limits at all on its efforts to falsify financial asset prices in order to “stimulate” GDP and its components; and any traditional notions of financial discipline and sound money.

As a practical matter that meant that interest rates could never be low enough and that risk asset prices needed to climb indefinitely and to be propped up by the central bank if they should seriously falter, as happened in 1987, 1998, 2000-2001, 2008-09, and essentially continuously ever since.

At length, of course, Keynesian central bankers have tumbled so deep into the monetary rabbit hole that they have lost all contact with the absurdity and danger of what they are doing. That is to say, they are massively and fraudulently monetizing the public debt and, increasingly, a rising share of other financial assets as well.

The BOJ owns 78% of Japanese ETFs, for example, the Bank of Switzerland is one of the world largest equity hedge funds and the ECB is a proud owner of hundreds of billions in corporate and junk bonds.

In all, led by the Fed, the Keynesian, price-targeting central banks of the world have undertaken a collective money printing spree that has not even a remote historical precedent—-with their balance sheets rising from $4 trillion to $25 trillion over the span between 2003 and the present.

Needless to say, every dollar of liabilities which funded that $21 trillion expansion was plucked from thin air. That is, it consisted of central bank confected digital credits which were used to purchase trillions of government debt from dealers and investors, and to then sequester those bonds and other securities on the balance sheets of the central banks, as depicted in the graph below.

That did tip the supply/demand balance—and mightily so—in favor of far higher bond prices and lower yields than would have resulted had the soaring public and private debts of the US and other nations been financed honestly out of the limited pool of private savings.

Combined Global Central Bank Balance Sheets

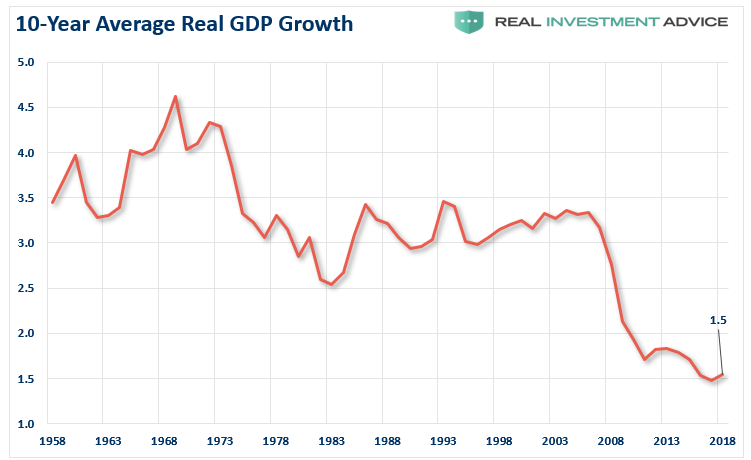

And that get’s us to the heart of the matter. Keynesian central banking is all about falsifying the price of credit and subsidizing the use of debt and leverage. And that’s notwithstanding the obvious real world proof that ever higher levels of debt and leverage relative to income have caused the growth rate of GDP to fall relative to history, not improve.

Stated in the inverse, contemporary central banking is not much about banking and money in the traditional sense. To our knowledge, there hasn’t been a single mention of M1, M2 or any other manifestations of money in the Fed’s post meeting statements and minutes in decades. Nor does the monetary politbur0 FOMC ever spend more than a fleeting moment on the condition of the banking system and the growth rate of bank deposit money (as distinct from hand-to-hand currency).

Accordingly, what is left in the financial system is credit, and the central banks have become its principal manufacturer in two ways.

First, the $21 trillion of central bank credit growth since 2003 shown above entered directly into the financial system, where it ultimately funded claims on labor, capital and materials. But in the first round it simply enabled government bond dealers to convert their cash receipts from selling QE bonds to the Fed into corporates, equities and other generally higher risk financial assets.

Secondly, the resulting rise in the price of corporates, equities and other risk assets purchased by the Wall Street dealers permitted these same money dealers to hypothecate them. That is, use the rising collateral value of these securities via margin loans and options and futures contracts to generate new credit without any bank intermediation or bank reserve increases at all.

In short, Keynesian central banking has now become the handmaid of a massive worldwide explosion of debt that has taken the level outstanding globally from $40 trillion in 1995 to $85 trillion on the eve of the 2008 financial crisis to $250 trillion today.

Needless to say, the stable and healthy historic ratios of debt-to-income have been blown sky high, rising from 150% in the pre-Greenspan era to 350% on average around the world today.

This dangerous decoupling of the real economy’s output and income from the outstanding level of debt and financial assets is plain as day when you look at central bank balance sheets relative to national income.

In Part 1, for example, we showed that since 1999, the bank of Japan’s balance sheet has risen by 604% compared to a mere 5% gain in the yen value of Japan’s nominal GDP. And as we also indicated, Japan is no single case aberration or even outlier.

Here is the same picture for the ECB and the eurozone GDP. That is, since 1999 the ECB’s balance sheet is up by 575% compared to a 77% gain in nominal GDP.

Nor is the US situation any different. Since 1999, the Fed’s balance sheet has grown by 1000%, while nominal GDP is up by just 110%.

Needless to say, this massive expansion of central bank balance sheets has caused the world to be inundated with debt and speculation, and to become shorn of the historical mechanisms of honest price discovery and discipline in financial asset markets.

So, to return to David Rosenberg’s question of the morning. Is there a chapter missing from Graham & Dodd?

Why, yes there is. It’s the scourge of Keynesian central banking that, ironically, arose from the monetary errors of the self-described slayer of Keynesian economics, Profesor Milton Friedman himself.