It doesn’t get more ridiculous than the Fed’s secondary market corporate credit facility (SMCCF). The facility is managed by BlackRock and “equitized” (viz. partly funded ) by the US Treasury, and could spend up to $250 billion buying existing corporate bonds with fiat credits snatched from thin digital air.

So far the SMCCF has spent nearly $430 million on the individual bonds of 85 companies and $6.8 billion on the pooled bonds embedded in exchange-traded funds. But when you look at the list of Fed holdings, the only thing you can really do is sputter, WTF!

After all, it includes such needy supplicants as Berkshire Hathaway, which is sitting on $173 billion of cash, as well as the likes of IBM, Comcast, Boeing, Exxon Mobil, General Electric, AT&T Inc and Pfizer. The list also includes the US divisions of numerous foreign companies including Japanese automaker Toyota and British energy giant BP.

These are all now or have been AAA companies!

Needless to say, the whole SMCCF operation is an outrageous windfall gift to corporate bond speculators on Wall Street, and an even more pernicious reward to unhinged financial engineering in the C-suites of corporate America. It has absolutely nothing to do with helping main street, fighting the Covid or any other of the risible excuses offered by JayPoo and his camarilla of group-think intoxicated monetary central planners.

Just consider the venerable AT&T Inc, which was the #1 individual corporate bond holding on the Fed’s recently disclosed list. That this giant financial engineering machine needed or deserved help from the central bank in assuring a “smoothly functioning market” for its debt securities—the ostensible reason for the Fed’s purchase of its bonds—is made a mockery of by the company’s Q1 financial results.

To wit, during the quarter in which the US economy was plunging into the swiftest, deepest recession in modern history, the company posted net income of $4.963 billion but saw fit to pay $3.737 billion in dividends and purchase $5.463 billion of its own stock.

You really can’t make this stuff up. In Q1 alone, the company cycled $9.2 billion or 185% of its net income back to Wall Street–even as it further trashed its balance sheet, raising its outstanding debt from $176.1 billion on December 31 to $185.0 billion as of March 31.

Once upon a time, there was an honest discussion about the inherent moral hazard fostered by the Fed’s market interventions, but what they are doing now is just flat-out jumping the shark. Why in the world would the central bank even think about goosing the bond prices of a company’s whose board of directors and executives are behaving with such reckless abandon?

We mean these cats have been conferred quasi-monopoly utility franchises by the state and have a market cap of $213 billion. If they thought the cost of bond financing in an honest debt market was too steep, they could always issue new equity for whatever financing contingencies AT&T might face.

Of course, the Wall Street stock speculators wouldn’t have been thrilled with the dilution implicit in that sort of honest financing alternative, so they brayed for more Fed “support” of the debt markets. And within days of the Covid Lockdown, they had lured the financial nincompoops who reign at the Eccles Building into this unconscionable exercise in wealth transfers to the tippy-top of the economic ladder.

In the case of AT&T that amounted to a stupendous reward not only for the financial folly embedded in its Q1 financials, but actually for a decade of the same. That is, since the first quarter of 2010 AT&T has generated $153 billion of cumulative net income, but has cycled fully 98% of that back into dividends ($116 billion) and stock buybacks ($34 billion).

But here’s the rub. This net income was purchased by $200 billion in acquisitions culminating in the $110 billion (including debt) purchase of TimeWarner. But if it spent all of its net income on dividends and buybacks, how did the company fund the $73 billion cash portion of its M&A spree?

No surprise there! By edict of the Fed, cheap money was literally flowing from the bond pits like milk & honey.

So AT&T raised its debt from $66 billion in Q4 2010 to $184 billion in Q1 2020 (which figure has since ballooned to more than $190 billion) to finance the $73 billion cash portion and tens of billions more of assumed debt in the M&A deals.

As telecom analyst Craig Moffett observed, “AT&T is the most indebted non-financial company the world has ever seen.”

Then again, exactly what did this massive debt-financed expansion of the company’s girth and improbable rise as a giant in the entertainment industry actually accomplish?

Nothing!

The net income of AT&T posted at $19.8 billion in 2010, which bottom line ended-up 27% smaller at $14.4 billion in 2019.

At the same time, AT&T’s asset base had exploded by 105% from $269 billion in 2010 to $551 billion in 2019. Lest it be wondered how profits essentially flat-lined and then eventually fell over the course of the last decade while the company’s asset base was growing by leaps and bounds, one need look no further than that dubious asset class called “intangibles and good will”.

That item soared from $134 billion to $304 billion over the period or by $170 billion, owing mainly to accounting entries for vastly over-priced acquisitions. By contrast, the company’s actual productive assets, measured as net PP&E (property, plant and equipment), rose by only $51 billion.

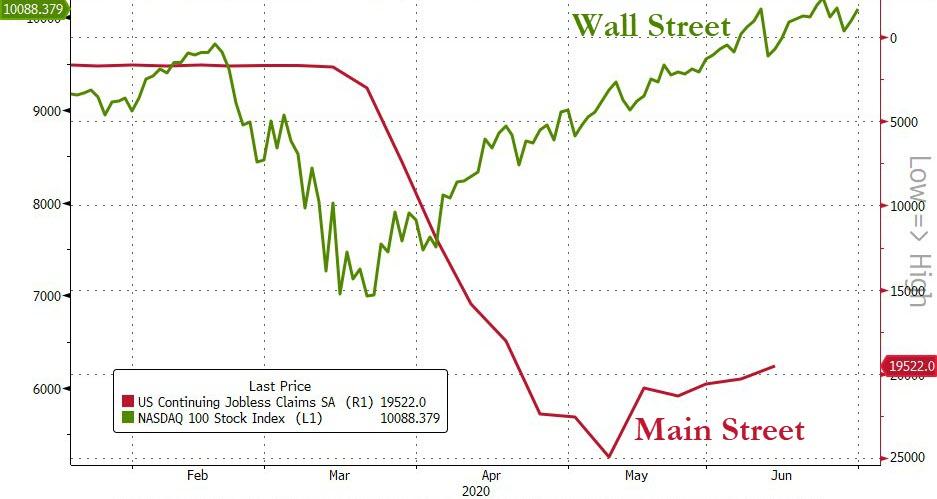

In other words, the Fed’s deep repression of interest rates has not been a tonic for productive investment and growth on main street; it’s been the fuel for rampant financial engineering that has lured the C-suites into the money dealing business—even as these digressions from the business of honest business building have deflated productivity and badly wounded and distorted corporate balance sheets.

At the end of the day, a $5.4 billion diminution of net income over a decade on the back of a $282 billion growth in total assets tells you all you need to know about the bogus economics of Keynesian monetary central planning.

And now these charlatans have actually doubled-down on their destructive handiwork of the past three decades by stopping cold any and all bond market price signals that might militate against further C-suite financial folly like that embedded in the tattered finances of the once and former Ma Bell.

Another poster child for this kind of Fed fostered financial engineering folly is McDonald’s Corp, and it was on the Fed’s bond shopping list, too.

Here a recent expose by Forbes succinctly outlines the manner in which the Fed’s coddling and subsidizing of Wall Street gunslingers and speculators has led to an outburst of so-called shareholder activism, which, in turn, resulted in the strip-inning of corporate balance sheets in order to fund financial engineering.

The McDonald’s saga began before the 2008 crisis when hedge fund speculator, Bill Ackman, began agitating the Chicago-based burger behemoth to divest its 9,000 company-owned stores in order to fund $12.6 billion in stock buybacks. Of course, this financial engineering ploy presumed either that–

- the independent operators who were to buy these company stores were stupid mullets and would vastly overpay for the resulting income stream net of the royalties and rents they would pay to McDonald’s (i.e. they bought the franchise but not the building or burger ovens); or

- cheap debt would subsidize the cost of asset ownership to the franchisees such that they could make the cost of ownership artificially pencil out even if they overpaid for what had been company-owned stores.

Initially, the C-suite at McDonald’s was astute enough to recognize that swapping existing assets and tomorrow’s income streams for cash today that would be immediately seconded to Wall Street did not exactly pass a smell test of real, sustainable shareholder value creation; and that the company’s historic policy of owning thousands of its own stores had been based on business considerations that were beyond the ken of hedge fund spread-sheet jockeys.

But beginning in 2014, McDonald’s then chief executive, Don Thompson, began piling on leverage to fund share repurchases. A year later his successor, Steve Easterbrook, amped up Thompson’s strategy by selling company-operated restaurants to franchisees, just as Ackman had advocated.

Taken together, the massive added leverage and drastically shrunken asset base made seeming miracles of financial engineering pencil out.

To wit, from 2014 through 2019 McDonald’s paid $19 billion in dividends and repurchased $35 billion of its own shares. Not surprisingly, that $54 billion inflow to Wall Street vastly exceeded the company’s $31 billion of net income during the six year period.

On an honest free market, of course, that kind of self-liquidation—eating the seed corn—would result in sharply falling equity values.

After all, when you sell or encumber with debt $23 billion of existing assets over 5 years in order to distribute 174% of your earnings, it’s a corporate finance gambit which implies a plunging terminal value.

But not in the Fed’s world of falsified debt and asset prices. As Forbes noted,

The new and improved “asset light” McDonald’s no longer manages cumbersome assets; instead, it receives those payments and is sitting on tens of billions in debt.

That was just fine by Wall Street. McDonald’s became a hedge fund darling, its shares more than doubling during Easterbrook’s tenure, from 2015 to 2019. His reward was $78 million in generous pay packages over five years.

The risk added to McDonald’s balance sheet has been dramatic, however. In 2010, the company carried just 38 cents in net debt per dollar of annual sales, but by the time Easterbrook was fired in late 2019 amid news of a workplace affair, it had $1.58 in net debt per dollar of revenue.

Today its net debt stands at $33 billion, nearly five times greater than before the financial crisis. Its bonds are rated triple-B, two notches above junk, down from their A rating in 2015.

Moreover, today 93% of the 38,695 McDonald’s stores worldwide are operated by small entrepreneurs who cover maintenance costs and pay the parent company rent and royalties for the privilege of operating in its buildings, using its equipment and selling its food.

Good luck to them as the Covid and Lockdown tsunami cuts customer traffic and sales revenue to the bone. And as for the royalty and rental streams that feed the P&L of the asset light parent company, even more good luck to that.

But even then, the Fed wasn’t done. With most of its restaurants nearly empty during the pandemic, McDonald’s stock initially fell by almost 40%. Thanks to the Fed’s intervention, though, McDonald’s debt, which at first slumped to 78 cents on the dollar, recovered along with the stock, as the company quickly raised an additional $3.5 billion.

Still, the chart below speaks for itself. Since December 2013, McDonald’s debt has risen by 177%, its share price by 90% and its net income, which at the end of the day is the true measure of productivity and value creation, is up by just 3.9%.

That’s right. When its debt went from $14 billion to $47 billion over six years, its net income rose by the grand sum of $218 million. And the company ended up with a drastically weakened and hollowed out balance sheet, to boot.

As long as we are in the fast food lane, it needs be noted that Wall Street instigated financial engineering fueled by cheap debt has been nearly universal in this sector. As Forbes further essayed, the job done on Yum Brands, the $5.6 billion (revenue) owner of Pizza Hut, Taco Bell and KFC, makes McDonald’s look like a case of financial sobriety:

The startling truth, though, is that the burger giant’s leverage is actually modest compared to one of its foremost competitors, Yum Brands. After Greg Creed took charge as CEO in 2015, activist hedge fund managers Keith Meister, of Corvex Management, and Daniel Loeb, of Third Point, took big positions.

By October of that year, Meister was on Yum’s board of directors; days after his appointment, the company said it was “committed to returning substantial capital to shareholders” and spinning off its Yum China division, which generated 39% of its profits.

Over the next year, Creed borrowed $5.2 billion to fund $7.2 billion of stock buybacks and dividends. Yum retired some 31% of its common shares, and as expected, its stock price doubled to over $100 by the end of 2019. Shareholders were thrilled, but Yum’s financial staying power was severely compromised.

In 2014, Yum had just $2.8 billion of net debt, accounting for 42% of net revenue; by 2020, that figure had swelled to $10 billion, or 178% of net revenue. Heading into the coronavirus economy, Yum was a basket case, but thanks to the Fed and a $600 million bond issue in April, it will live to see another day.

In Part 2 we will further document that folly of the Fed’s new mission of explicitly goosing the price of corporate bonds in order to keep yields ridiculously and artificially low.

But with even BBB bonds yields, which are border line junk, now at just 3.59% in the face of the greatest economic plunge in modern history– it can be well and truly said that the zombification of corporate America is irretrievably underway.

In this context, David Rosenberg said it as well as possible in his morning missive:

Further to this, I have to say that if you are trying to identify how the Fed has exerted a monumental impact on the financial markets, consider that U.S. investment grade rated companies issued a massive $840 billion of bonds in the first half of the year,which included the worst recession since the 1930s —that number is so big that it matches the previous full-year record established in 2017 and is about double the prior first-half record set in 2016.

The Fed’s backstops and interventions allowed non-investment grade issues (junk) to float an absolutely stunning $180 billion,which also tops the previous first-half record in 2015.

What is even more amazing is that the investor demand has been so frenetic that the average yield on investment grade bonds since March 20th has collapsed from 4.7% to new all-time lows of 2.2%!

Truly an insane level of risk compensation if Jay Powell is correct in his assertion of elevated uncertainty levels—normally, investors in corporate credit would want to be paid to take on risk, but in today’s world where everyone believes the Fed,or the Federal Government,will bail you out, investors don’t seem to mind paying the borrower for the risk. A recession where risk-premia melts away… a new one for the CFA textbooks.

In fact, if the Fed allowed markets to clear on their own and reflect decade-high default rates, the high yield interest rate today would be north of 10%.•

This is the end-result of collective guilt at the elected government level for shuttering the economy and for not being adequately prepared for the pandemic.

But we have to keep in mind that wages earned through work is not the same thing as borrowed money being doled out by the government and treated as “income”in the BLS reports —one reflects income from labor productivity; the other is debt-financed social policy with zero productivity payback.

Perhaps the price to keep society functioning. But there is no such thing as a free lunch, and the government may well be adept at redistributing income but has no ability to create income.The fiscal situation is a complete mess and,unlike the late 1940s, there are no troops coming back home to stimulate demand and help the country “grow”out of the debts needed to defray the cost of WWII.

It could not be better said. Nor does this chart leave any confusion about whom calls the tune in the Eccles Building.