We might as well start with some gibberish—this time from San Fransisco Fed president, Mary E. Daly:

Raising rates now could be premature. It could leave the economy short on both price stability and employment.

Truly. How do they get away with such tommyrot?

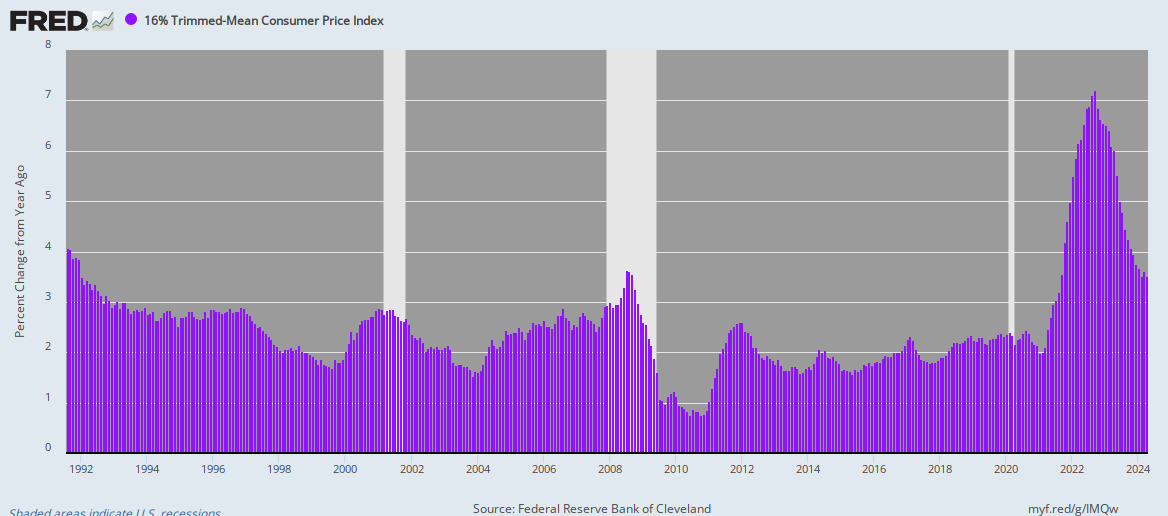

As to price stability, take a look at the graph below. It tracks the 16% trimmed mean CPI since it last equaled October’s 4.1% y/y gain back in August 1991. The average annual gain since then has been 2.31% for 30 years running; and since the Fed officially embraced the damnable idea of targeting 2.00% inflation in January 2012, the annualized gain has been 2.21% per annum.

So where is the want of 2.00% inflation, assuming that’s a swell objective, which it most definitely is not?

Really, you can’t get any better measure of the long-term inflation trend than the 16% trimmed mean CPI. That’s because month-after-month it throws out the highest and lowest 8% of price change outliers, thereby insuring that the underlying trend of the overall CPI market basket is consistently reported.

Y/Y Change In 16% Trimmed Mean CPI, 1991-2021

As per the Fed’s vaunted “employment” objective, riddle us this: When the Virus Patrol closed down the restaurants and bars in April 2020 and the job count in that sector plunged from 12.308 million to 5.975 million or 48% in two months, what did “aggregate demand” have to do with it? How could the Fed’s demand-focused tools have done anything to remedy it?