In March 2007 Bernanke infamously proclaimed that the US economy is in a good place and that—

“…..the impact on the broader economy and financial markets of the problems in the subprime market seems likely to be contained.”

There must be something in the water cooler at the Eccles Building because surely Powell has just had his Bernanke moment. In countless ways, the US economy stands directly in harms’ way, but the empty suit that heads the Fed was having none of it in his Congressional testimony today:

The U.S. economy is now in the 11th year of this expansion, and the baseline outlook remains favorable…. Looking ahead, my colleagues and I see a sustained expansion of economic activity, a strong labor market, and inflation near our symmetric 2 percent objective as most likely. This favorable baseline partly reflects the policy adjustments that we have made to provide support for the economy.

We bolded the 11 year expansion and the self-congratulatory “policy adjustments” clauses for a simple reason: How in the world can the “outlook remain favorable” after as 12-year period when the Fed has expanded its balance sheet 7X faster than the growth of nominal GDP?

That’s right. The nominal GDP at $21.5 trillion today is 45% larger than it was on the eve of the financial crisis in Q4 2007, but the Fed’s balance sheet has metastized by 330%, and now these fools have it growing again via “not QE”.

Here’s the thing. The $3.1 trillion growth of the Fed balance sheet during this period was not the monetary equivalent of a tree falling in an empty forest. Accordingly, the 125-month long simulacrum of an economic expansion now stumbling towards its sell-by date is not your grandfather’s benign business cycle, either.

To the contrary, the Fed’s radical, unprecedented and unjustifiable flight into monetary crankery has profoundly changed everything in the financial and economic landscape. There is literally no financial asset price that has not been deeply impacted and falsified by this sustained spasm of money printing and interest rate repression.

Needless to say, that matters profoundly because financial asset prices are the signaling system of capitalism. They fundamentally impact borrowing, saving, investing, allocation, efficiency and speculation.

But when the signaling system is falsified, you inherently get excessive speculation, leverage, malinvestment, imbalances and dangerous financial bubbles. And eventually that leads to financial crises and body blows to the main street that are unnecessary, unjust and irreversible.

By the facts and Powell’s own admission, for example, aggregate economic growth is being held-down by flagging productivity and sub-normal labor force participation rates. The Fed Chair even admitted that US participation rates are among the lowest in the developed world.

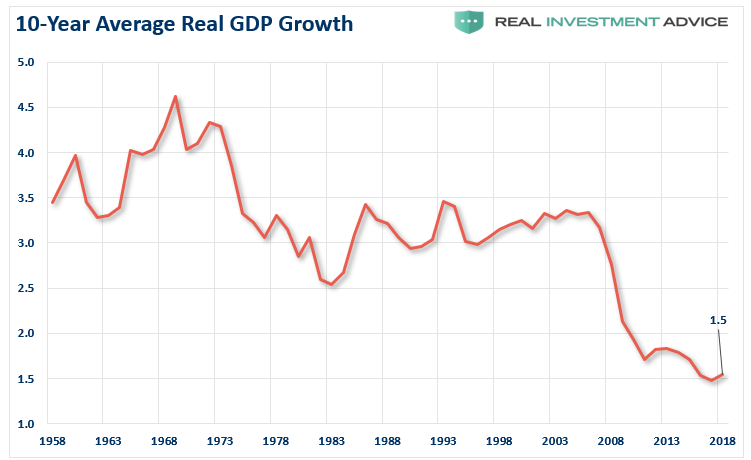

As a matter of pure GDP mechanics (growth of labor hours + productivity=real GDP), therefore, it is no wonder that the 10-year smoothed trend of real GDP growth has literally been cut by two-thirds. And that has happened, once more, in a world in which the raw ingredients of potential labor supply and technological innovation have rarely been so abundant.

So the question recurs: Have these radical Fed policies affected behavior in the corporate sector?