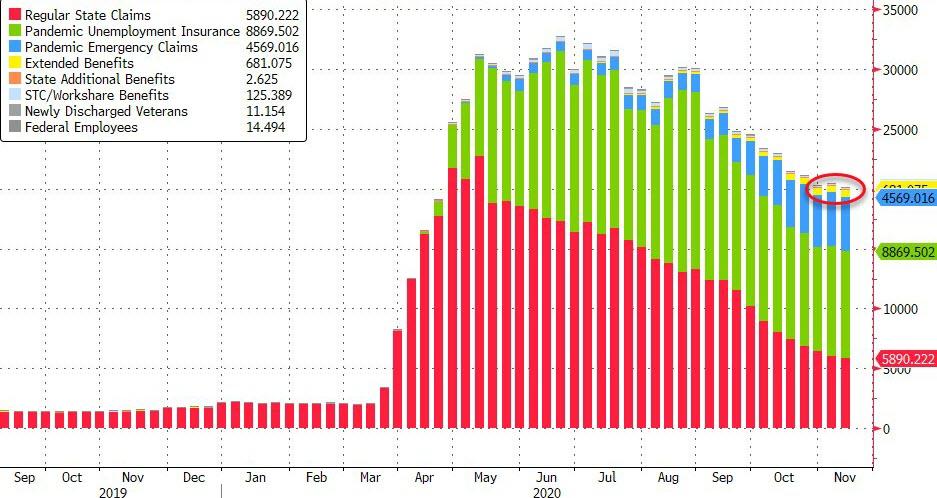

On Thursday, the government said there were still nearly 20.2 million unemployed Americans drawing UI benefits. That’s almost 13% of the work force, and included 5.8 million under regular state UI programs, 14.1 million under the federal emergency pandemic programs and 0.2 million under certain veterans, Federal employee and other programs.

Compared to bubblevision’s ballyhoo about a steadily recovering labor market, the chart below, which includes all 8 categories of state and Federal UI benefits, amounts to a bucket of cold water—even if it is down from the thundering peak of 32.44 million claimants back in June.

The reason the MSM doesn’t get it, of course, is that we are once again dealing with the horrid Recency Bias that stems from the 24/7 news flow and the core establishment narrative that everything is now awesome or soon will be.

Not at all. Here are the peak levels of unemployment claims during the previous four recession cycles. The June peak was 5X the worst week of the Great Recession and after months of alleged booming jobs recovery is was still 3X the June 2009 high.

Peak Unemployment Claims During Prior Recessions:

- June 2009: 6.534 million;

- January 2002: 3.529 million;

- June 1991: 3.473 million;

- November 1982: 4.637 million.

Needless to say, this chart is the Virus Patrol at work. It put 30 million + workers on the unemployment dole for more than 10 weeks running and more than 20 million continuously for the last eight months.

It’s also the reason the big spenders of both parties are inching toward a $1+ trillion Everything Bailout 5.0 on top of the $3.5 trillion already enacted.

In effect, the chart below depicts the massively expensive flow of transfer payments that have kept the macro-economy floating on an air cushion of free stuff. It’s also depicts the Washington created “fiscal cliff” that hangs over the main street economy like an economic Sword of Damocles.

If and when the Fed UI bailouts are allowed to expire (now December 31), for instance, 14 million unemployed workers (green and blue portion of the bars) will be left high and dry.

Today, of course, the Labor Department reported a wholly different “Jobs Friday” figure, which promptly induced the Robin Hood mullets to buy even more over-priced stocks.

Likewise, at least according to Kudlow, the November jobs report was just further evidence that the Ever Trumpers were right to believe that the Donald has engineered a great “V” rebound, even if his apparent Oval Office eviction notice holds up in the courts.

To be sure, the, the November report showed just 243,000 new jobs and represents a sharp and continuing deflation of the large gains recorded during May and June.

But both the White House and the Wall Street cheerleaders know how to spin a half empty glass when the see one. Folks, we’ve had an all-time record gain of 12.24 million new jobs during the last seven months. Surely, the “V” doth cometh.

Nonfarm Payroll Gains, May-November 2020

In truth, of course, the, blue bars above represent “born again” jobs, not new ones. And after seven months of the most massive fiscal and monetary stimulus in the history of mankind, they collectively signify the rebirth of just 55% the 22.2 million job lost owing to the Virus Patrol’s lockdowns, quarantines and fear quotients administered during March and April.

More importantly, they signify that what was already a listing, structurally impaired economy back in February—the antithesis of MAGA—and which was knocked flat-on-its ass by the lockdowns, is still struggling to get up off the mat.

In fact, the 142.6 million payroll jobs reported for November represent a 5-year retreat to the level first reported in October 2015, and only a 3.1% gain from where the US jobs count stood at the peak of the pre-crisis expansion in November 2007 (138.3 million).

Here’s the thing. Historically, more than half of GDP growth has come from increased labor inputs and the balance from productivity gains. But as of November 2020, jobs growth since the pre-crisis peak (Nov. 2007) amounts to just 0.24% per annum.

That’s right. You can’t get rising prosperity—to say nothing of the capacity to carry today’s $81 trillion combined private and public debt burden—out of labor input growth that is barely a rounding error above zero.

Worse still, the Keynesian talking heads on both ends of the Acela Corridor claim that unless another $1 trillion Covid relief bill is passed pronto, we are heading back into a double dip recession and a retreat of employment levels from even today’s sickly totals.

So the question recurs. Why does anyone in their right mind choose to call the far right hand margin of the chart evidence of a bublicious “V”?

It’s actually a mark of severe trouble down in the plumbing of the main street economy, and implies a lot more to come. Its also a reminder that Jobs Friday is one of the great scams of all times.

They keep trumpeting “born again” jobs as if they represented new labor deployments, while always blanking out the history and longer-term trends—confident that the day-traders and re-election bent pols will never notice the difference.

Needless to remind, the initial establishment survey jobs count each month—as weak as the November figures were when viewed in context— isn’t worth the paper it is printed on. It is absolutely certain that by the time five year’s worth of model projections, estimates, imputations and benchmark revisions are completed, the final blue bars for the last seven months will not remotely look like what is displayed above

But our point is not merely that the initial BLS monthly jobs report (remember, it is largely a modeled projection, not a count) is an embarrassment and relic originally created by Francis Perkins’ New Deal social workers at the DOL and jerry-rigged by Keynesian economists and government apparatchiks thereafter.

Rather, the important point is that it is a propaganda tool and narrative-shaper, which especially at turning points and during crisis outbreaks, functions to keep a simulacrum of prosperity flashing on the media screens, when actually the bottom is dropping out of the debt- and speculation-riven economy that Washington has been midwifing for the past three decades.

As a technical matter, the basis for some of the gap between the “recovering jobs” market narrative and 20-30 million workers on the dole lies in the alacrity with which the Labor Department causes millions of unemployed workers to go missing.

When all else fails, the blue line in the graph below, which allegedly measures the “labor force”, can be counted on to partially square the circle. That is, if workers disappear from both the labor force and the unemployment rolls, the headline U-3 unemployment rate goes down.

Then again, the idea that the “labor force” declined from 164.55 million workers in February to 156.48 million workers in April is just puzzle palace stuff from the Washington data mills; and the fact that it still stands at just 160.47 million as of November is more of the same malarkey.

The fact is, the demographic counts and the number of able-bodied, or at least available workers in the 20-69 years cohort, did not change a whit during those eight months. That’s as in none, nichts and nugatory.

In this day and age, the potential labor force is the entire pool of 204 million adults age 20-69, reduced at various points by fluctuating numbers of early retirees, social security disability recipients, work-at-home spouses, students, welfare grifters and video-game jockeys in mom & pop’s basement.

The very idea that the BLS can parse all these categories as between labor force participants and non-participants is nonsense; and that’s especially true because the changing mix and incentives for work provided by transfer payments, student aid and the economics of two- versus one-worker households cause constant flux on the margin.

So the plunging blue line in the chart below, therefore, is just a quasi-random artifact of the BLS’ screwball methods for determining who is and is not in the “labor force” at an given moment in time and in the context of dynamically changing economic circumstances on the ground. But when you add these randomly disappearing workers in the monthly surveys to the BLS’ imprecise survey estimates of workers technically classified as “unemployed” each month, some of the gap closes.

For instance, at the April bottom, 8.065 million workers had dropped out of the labor force compared to the February pre-Covid level, while the BLS bean counters designated another 23.078 million workers as officially unemployed. So that amounted to 31.14 million workers not employed—a level pretty close to the steady-state level of UI beneficiaries shown at the time in the first chart above.

Of course, thereafter, the BLS bean counters miraculously found fewer and few workers had dropped out of the work force and also that fewer and fewer needed to be officially classified as “unemployed” (brown line). Thus, as of today’s report for November, the “labor force” shrinkage from February was down to 4.676 million and the number of officially unemployed had shrunk by 53% from the April level to 10.735 million.

So by the BLS’ lights there were a total of 16.5 million workers not employed in November who had been in February. As to the whereabouts of the other 4 million workers are who are drawing the UI dole, the BLS didn’t say and the bubblevision talking heads didn’t ask.

But wherever they are among the 203 million working age Americans, one thing is sure: There is not even a semblance of a labor market “V” recovery. Either that or we have UI fraud on a biblical scale.

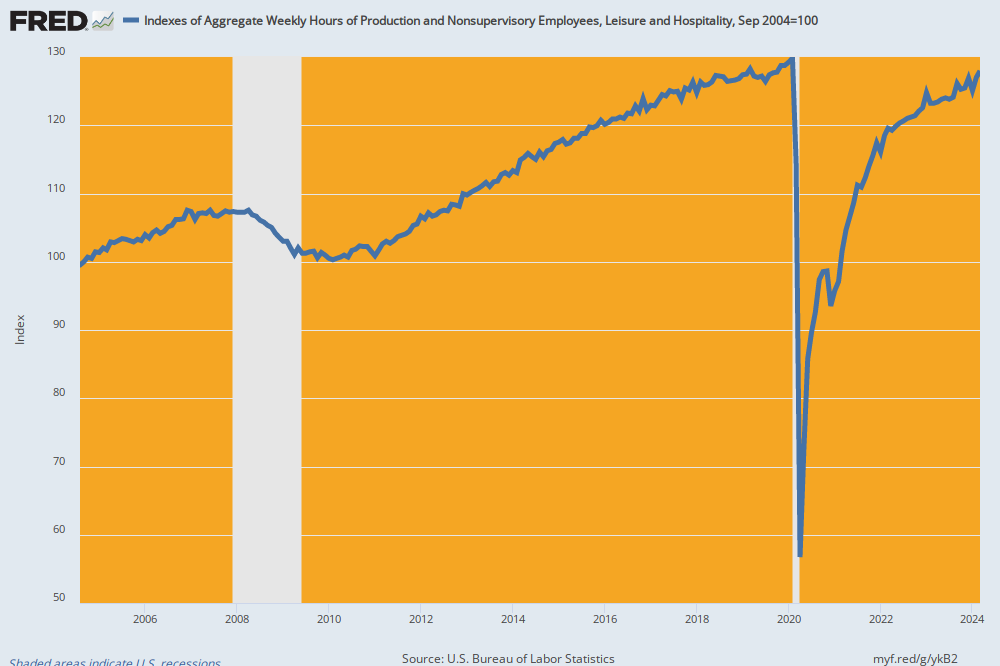

Yet, that’s not the half of it. The modern labor market works on hours, not a census of heads employed. After all, today’s “jobs” range from 10 hours per week in the part-time sector to 50 hours or more in heavy overtime situations.

So the relevant gauge of the labor market is the index of hours worked, which washes out the distortions from counting 10-hour per week gigs at McDonald’s the same as 50 hours per week on the factory floor or in the (remaining) coal mines.

So, yes, you can call the chart below evidence of a “V” on a paint-by-the-numbers basis, but what it really shows is the utter folly of Lockdown Nation and the unspeakable depths to which economic marshal law has driven the labor market.

To wit, between February and April, the index of private hours worked plunged by a stunning 19.0%—-a two-month monkey-hammering that has no precedent in the historic statistics, even during the Great Depression of the 1930s.

This meant that the US economy during April was employing the same number of labor hours as had been recorded way back in August 1997. That’s 23 years of retrogression in 60 days!

Moreover, notwithstanding the partial recovery since then, the fact remains that hours employed in November were still down nearly 6% from the February pre-Covid level, and actually were only 4.5% above where they stood way back in November 2007.

In short, 60% of all the ballyhooed labor hours growth reported month after month on Jobs Friday between the pre-crisis peak and February 2020 was still AWOL in today’s jobs report.

Moreover, when we look at the BLS’ hours employed indices for the social congregation sectors that have felt the brunt of the Lockdown Nation boot heel, the irrelevance of the “V” narrative becomes all the more evident.

The heart of the Lockdown hit the 17 million workers in the restaurant, bars, hotels, parks, movies, sporting events and other leisure activity venues the hardest. Accordingly, between February and April the index of hours worked in the leisure and hospitality sector plunged by a staggering 57.4%; hours worked that month were actually lower than at any time since April 1977!

That’s right. Dr. Fauci and the Virus Patrol in one fell swoop rolled back 43 year’s worth of employment gains in one of the few major sectors of the economy that has actually shown net job growth since the turn of the century.

So where did we end up in November?

Well, at the level first crossed in September 2004.

And, yes, 16 years of retrogression is better than 43 years, but it’s a “V” only in the paint by the numbers sense.

Paid hours in these social congregation sectors were still down in November by 23% from the February level; and with the new lockdowns and social controls now rolling across the nation, the still disastrous contraction of paychecks reflected in the November figure for the huge Leisure & Hospitality sector is not likely to improve anytime soon.

Aggregate Labor Hours Index: Leisure & Hospitality Sector, 2004-2020

The same story is evident in the health care sector—another huge piece of the social congregation economy. And as we have previously noted, that’s especially ironic because supposedly the reason for the Lockdowns was a medical crisis.

Nevertheless, after peaking at 16.507 million jobs in February, the figure dropped by 1.577 million or 9.6% in April, and still remains 530,000 jobs or 3% below the pre-Covid levels.

The point here is that for better or worse, the health care sector has been the motor force of jobs growth since the turn of the century, and had actually generated an average of 25,400 jobs per month over the 20 years through February 2020.

But now the Virus Patrol has knocked even the health care sector on its heels.

The story is the same in the education sector, and given the intense pressure against school re-openings at all levels of the education system, the trends shown below are not likely to improve materially at any time soon.

The chart tracks education sector employment by local governments (public school systems), state government (higher education) and the private sector from pre-K through private colleges and graduate schools. At the combined peak of 14.360 million jobs in February 2020, education sector employment had grown by 56% from the 9.21 million level recorded in January 1990.

But the Virus Patrol made sure that trend changed sharply. Total education employment was down by 1.16 million or 8.1% by April, and has continued to slide lower. As of today’s report for November, total education employment was down by 1.4 million or nearly 10% from its February level.

Again, with a new wave of lockdowns sweeping the nation, there is no reason to expect that the November levels will pick-up materially any time soon.

Total Employment, Education Sector, 1990-2020

At the end of the day, however, there is something even more ominous in the background of today’s so-called jobs report. Namely, after three decades of Keynesian central banking, the US has become a debt-ridden hand-to-mouth economy.

Upwards of 80% of households have no material cash savings or rainy day funds, and just since the pre-crisis peak, business debt has soared from around $10.1 trillion to $17.6 trillion at present. So with the labor market monkey-hammered by the Virus Patrol, all hell will break lose if the massive flow of Washington free stuff is interrupted or materially reduced.

For instance, 15 to 23 million renters are at risk of eviction if the current moratorium is not renewed and Washington’s coast-to-coast soup lines are not replenished.

Even the robust rebound of the goods producing sector has now relapsed to the flat line.

As we have previously observed, at cyclical turning points in particular, the U.S. jobs band gets especially irregular with the goods producing sectors–mining/energy, manufacturing and construction—falling by the wayside first.

Consequently, hours growth in the goods sector had already lapsed to the flat-line during 2019, reflecting the end of the tax cut tailwind and the intensifying headwinds being generated by the Donald’s Trade Wars. But then it literally plunged down the shaft during the original March and April 2020 lockdowns, falling by 19.1% on a year-over-year basis during the April bottom.

Self-evidently, the “V” rebound has stalled out, with total hours worked in the goods producing sector still 5.5% below year ago levels.

But that’s not the half of it. The index of hours worked in the goods sector for November was actually 6.8% below another benchmark: Namely, the level first achieved 72 years ago in January 1948!

Honest injun! Total hours employed in the high productivity sectors of the US economy, which is reflected in an annualized pay rate of $62,660, are lower than they were when Harry Truman was fixing to give the Republicans hell during the 1948 election.

So enough of the “V” already.

As it happened, the November figures represented a 60% recovery from the deep April jobs losses for both the good-producing sector and the leisure and hospitality sector. That’s fittingly symbolic because it captures in a one-month snapshot the egregious imbalance that has accompanied the entire recovery since the Great Recession.

Job Gains Since the April 2020 Lockdown Bottom:

- Good Producing Sector: +1.539 million or 61%;

- Leisure & Hospitality sector: +4.869 million or 59%

However, as today’s report also shows, average weekly earnings in the good-sector last month were $1,205, which equates to an annualized wage of $62,660. By contrast, average weekly earnings in the bar/restaurant/hotel/sporting arena sector was just $439, which equates to an annualized wage of $22,828.

So from an aggregate income point of view, these Leisure & Hospitality gains amount to 36% jobs.

So on an annualized run rate basis, the November job counts in these two categories relative to the April bottom compute to a $96 billion pick-up for the goods-producing sector and just a $111 billion annualized rate of recovery for the Leisure & Hospitality sector—notwithstanding a 3.2X larger gain in the job count.

Either way, that’s not exactly winning, and it surely isn’t Awesome.

Nevertheless, that’s the essential story of the current so-called recovery. Relative to the pre-recession peak in November 2007, the count of “36% jobs” in leisure and hospitality has essentially recovered to the flat-line at 13.4 million jobs, while goods-producing jobs are still 8% below their pre-recession peak.

Again, in dollars of income, the implications are startling. At November weekly earnings rates and employment levels, the goods-producing sector generates $1.268 trillion of wages on an annual basis and the Leisure & Hospitality sector generates just $306 billion.

So as we said, their ain’t nothing Awesome about the US jobs market. Jobs Friday, in fact, is just one great big cover story for a casino that has become total unhinged.

Total Employment, Good-Producing and Leisure & Hospitality, 2007-2020

To be sure, the Jobs Friday con has been going on for years, but that does not gainsay the deteriorating trend that the Wall Street/Fed narrative total obfuscates.

Jobs are migrating from goods to services and from high pay to low pay, but at some point soon the US economy is going to run out of tax dollars and borrowed money to fund the growth of households’ doing each others’ laundry.

To repeat, during November 2020 on an annual basis goods-producing jobs were worth $62,600, health and education jobs were worth pay of $48,500 and hospitality and leisure jobs were worth $22,820.

Yet since January 2000, the total number of good-producing jobs has shrunk by –17.8%, while leisure and hospitality jobs are up by +14.5% and health and education jobs by +54.3%.

You could call that running-in-place rather than Awesome and be done with it. But there is actually a further even more vexing angle with respect to the trends embodied in the chart below. To wit:

- Households with incomes of $100,000+ account for nearly 50% of restaurant spending and own nearly 90% of the stock. When the bubble bursts, so will their spending.

- Upwards of 90% of the $5.0 trillion spent on health and education services in the US is provided directly and indirectly by the public fisc. The latter is going broke fast, and so is its ability to fund the growth of services and jobs in the HES complex.

At the end of the day, the real Big Lie of the present time is that the labor market is rebounding in an awesome “V” and it will keep the GDP cranking ever higher.

In fact, today’s Jobs Report proved once again that nearly the opposite is actually the case.

t