Pocahontas and the Dem papooses still in the race talked up the wealth tax last night, but we are not sweating for the nation’s 605 billionaires. Half of them apparently wish to do it to themselves, anyway.

But we are wondering when the great unwashed masses are finally going to get the joke. The overwhelming reason there are 605 billionaires qualified for Elizabeth Warren’s 3% wealth tax and 83,500 households with net worths over $50 million and thereby qualified for the 2% wealth haircut (per year!) is the 12 knuckleheads domiciled in the Eccles Building

The latter have spent decades inflating the hell out of US financial assets—a truism that the chart below validates in spades. To wit, central bank “stimulus” has caused household financial assets to grow at twice the rate of income growth for the past 32 years running.

That is not the free market at work. No way. No how.

What the chart means is that the capitalization rate of the US economy has doubled since Greenspan’s arrival at the Fed in mid-1987—even as the growth rate of the US economy has fallen by two-thirds from its historic norm.

Thus, in 1987 household financial assets of $13 trillion represented 2.7X national income (GDP) of $4.8 trillion, but by Q2 2019, financial assets had exploded to $91 trillion. That represented 4.3X current period GDP of $21.3 trillion.

Stated differently, had this massive valuation creep and financialization of the US economy not occurred in the interim, household financial asset holdings would currently total about $58 trillion at the pre-1987 ratio to GDP.

The $33 trillion difference is the dubious wealth “gift” of the Fed and the other major central banks of the world.

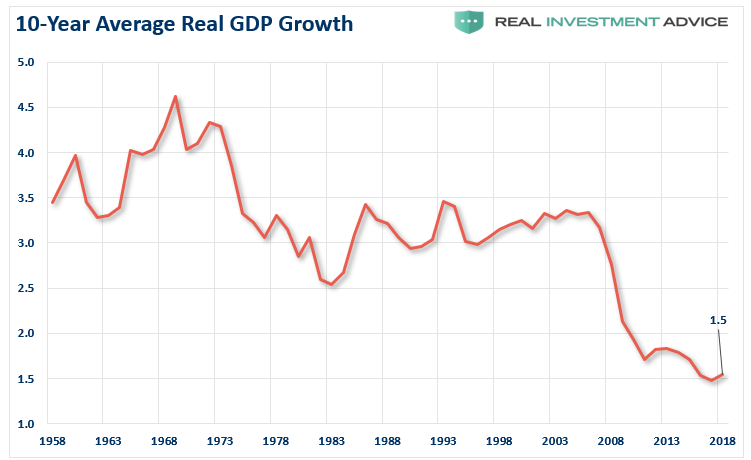

And we do mean “gift”. After all, the US economy is on an unmistakable downward trajectory of ever slower growth. And the chart below screens out all the short-term inventory fluctuations and cyclical dips and rips by tracking the 10-year rolling average rate of GDP growth.

The implication can not be gainsaid. A 10-year trend growth rate of 1.5%—and which is likely heading lower after the impending recession quarters are rolled in during the early 2020s—should be capitalized at a lower multiple than was the pre-Greenspan economic growth rate of 3.0% to 4.5% per annum, not a sharply higher one.

Moreover, and for want of doubt, the above displayed inflation of the capitalization rate did not begin until after Greenspan took the helm at the Fed in August 1987.