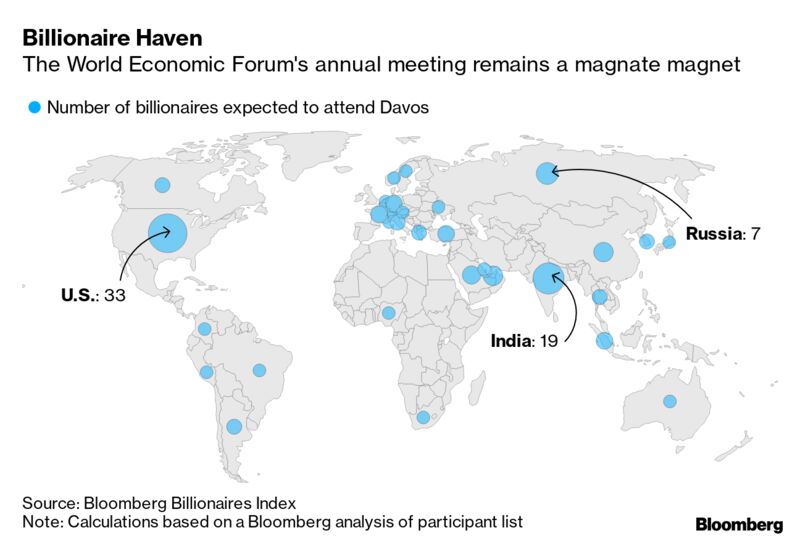

There are a reported 119 billionaires attending the Davos confab this year—plus (allegedly) the Donald, who took a day off from Impeachment to address this august gathering of the world’s movers and shakers.

There is also 1500 private jets crowding the surrounding airports—plus the notable train-traveling 16-year old expert on planetary climate science, Greta Thunberg.

Also, among the 10 billionaires in attendance from communist China is Ren Zhenfei, founder of Huawei and father of its CFO, Meng Wanzhou. Even as dad courts the rich and famous on the slopes, daughter languishes in a Canadian jail waiting extradition to the US because she had the audacity to do business with Iran against Washington’s instructions and Trump’s latest fatwa against the Tehran government.

These odd juxtapositions plus countless more got us to thinking about Davos Man himself and the ultimate juxtaposition of our times.

To wit, the combined net worth of the world’s billionaires in the year 2000 was $1 trillion, according to Forbes, but at this bublicious moment that number is reckoned at just under $10 trillion. So the 2,150 members of the Billionaires Club now have more net worth than 60% of the world’s population combined. That’s 4.6 billion people!

In so noting, of course, we are not joining the Bernie Sanders/AOC/Pocahontas brigade. In a world of free markets, honest money and de minimis government, the more billionaires the better. But what we sincerely doubt is that there was an honest and sustainable basis for a 10X gain in the net worth of the Billionaires Club over a two decade period when the world’s nominal GDP only rose from $35 trillion to $85 trillion, or by 2.4X.

After all, the predominately financial assets comprising the world’s net worth are merely the capitalization of its underlying income or GDP. And there is no basis in either sound economics or basic math for the former to grow nearly four times faster than the latter for two decades running.

Stated differently, unless the age-old laws of sound money have been repealed by the economic gods themselves, Davos Man is fixing to become nearly as rare as Neanderthal Man or, more to the point, has been a case of Piltdown Man all along.

Recall that the latter had been touted by some British scoundrels in 1912 to be a 500,000 year-old homo sapiens and evolution’s missing link. Alas, it was actually a ho-hum 50,000 year-old human skeleton fused with the jawbone and teeth of a modern orangutan.

As it happened, it took the world about three decades to figure out that Piltdown Man was a hoax, but the hoax attendant to Davos Man is already plain as day. That’s because by even tolerating Greta’s impending extinction hysteria and the Donald’s hideous Greatest Ever Economy boasts, the assembled billionaires are demonstrating that they are not 4X geniuses after all—just bubble riders on the great central banking hoax of the 21st century.

Indeed, we would suppose that some kind of guilt-tripping would account for the grandly named World Economic Forum’s (WEF) solicitude for the global warming scam and its intellectually pre-pubescent poster girl, Greta. But why in the world would the purported deep thinkers of the WEF not laugh the Donald’s malarkey right off the stage?

On the way to Switzerland he tweeted a superlative that would be the envy of the biggest braggart in the school yard:

“We are now NUMBER ONE in the Universe, by FAR!!…….

And then he thickened the goo while at the podium in Davos:

America’s newfound prosperity is undeniable, unprecedented and unmatched anywhere in the world…America made this stunning turnaround not by making minor changes to a handful of policies but by adopting a whole new approach. Every decision we make…is focused on improving the lives of every day Americans. We are determined to create the highest standard of living that anyone can imagine.”

Folks, that’s just blithering poppycock. We are at the end of the longest and weakest business cycle expansion in history (month # 127), yet real median household income has barely returned to where it stood two decades ago.

The idea that Trump-O-Nomics has anything to do with paving the way for the “highest standard of living that anyone can imagine” is just content free bluster.

The facts actually show that the US standard of living has been stagnant for two decades, rising and falling with the business cycle, but gaining on average the grand sum of $87 per year (2018 $) since 1999.

That’s right. As shown in the graph below, the $63,179 median reported for 2018 is undoubtedly the high water mark for years to come, yet it representd a mere 2.7% gain from the $61,526 level (2018 $) posted way back in 1999.

While the data for 2019 is not yet available, it is evident that the various categories of income gain last year barely kept up with inflation, meaning that real median family income was flat. So the coming recession in the early 2020s will send the black bars in the chart sliding lower as they did during and after each of the recessions marked by the white space.

Here’s the thing. The Donald’s policies have immensely harmed the foundations on which today’s tepidly expanding business cycle rests. Yet there has been no short-run benefit in terms of accelerating overall GDP growth, and actually a sharp deceleration of business investment and export growth.