The stridency and blatancy of the Donald’s attacks on the Fed are without precedent, but you haven’t seen nothing yet. When the third great bubble of this century cracks, and the Dow, GDP and jobs plunge southward, the Donald will wage war against the Fed with such ferocity as to make FDR’s infamous 1937 packing attack on the Supreme Court look amicable by comparison.

And there is no mystery as to why. America is caught up in a monumental economic and financial fantasy that is just one stock market meltdown away from collapse. Yet if another devastating recession engulfs main street America during the next 15 months, the Donald will be bitterly blamed (fairly or not) and be hounded from office in a landslide in 2020—-even if the Dems run Sleepy Joe or Mickey Mouse, as the case may be.

The Donald is a dumbkopf when it comes to economics and most other policy matters, but he’s a proven genius when it comes to survival. He knows full well that if the Dems win the next election, he will be viciously prosecuted and sent to the Big House for the remainder of his days.

The Donald’s other—and intimately related—great talent is that of a take-no-prisoners street fighter par excellence. And that means that if the stock averages and GDP/jobs metrics begin to falter even modestly, the Donald will go on a relentless, incendiary, bellicose attack on the Fed designed to keep the bubble alive and forestall his own demise.

So whatever he accomplishes during his flukish tenure in office, the most important by far will be to puncture and discredit the hoary notion of independence and technical expertise that underpins the Fed.

That is, the canard that it is some kind of monetary college of cardinals, possessed of extraordinary skill and virtue in the art of financial and economic management and positioned far above the fray of ordinary democratic governance and the coarse partisan politics that attend thereto.

No, no, no!

Actually, the Fed is no more essential to American prosperity than the Tea Tasters Board of yore, and it is one of the most base, arrogant, power-aggrandizing institutions ever to rise on the landscape of modern governance.

Contrary to the myth of apolitical technocracy and independence, the Fed is egregiously political from top to bottom. Except its politics are those of an elitist economic ideology, not the rambunctious partisanship of Dem versus GOP.

But for the most part, the latter kind of partisan politics is a relatively harmless indoor sport. The Founding Fathers were overwhelmingly skeptical of the state, if not downright hostile. They therefore confected a machinery of Federal government that was designed to slouch toward inertia and inaction and to function as a forum for the demos to let off steam, not tread heavily upon the liberty and enterprise of a free society.

Needless to say, they did not anticipate the creation of a powerful central bank that would escape entirely the multiple layers of checks and balances that pertain to the other branches and institutions of the American state. Yet that is the essence of the matter: The Fed embodies a financial dictatorship run by an unelected, essentially self-perpetuating elite that amounts to a monetary politburo.

Of course, dictatorships everywhere and always fail because they offend the natural rights and liberties of free peoples and are incapable of economic calculation—-the very province of the free market that makes prosperity possible.

In the case at hand, the monetary politburo’s economic infirmities are every bit as severe as the Gosplanners of the Soviet Era or the giant lumbering state companies, banks and state bureaucracies of the Red Ponzi. Like them, the Fed pretends to allocate trillions of capital and credit, yet has no capacity to efficiently price it.

Indeed, socialism never even figured out how to efficiently produce and distribute municipal electric power, price the collection and disposal of household trash or operate local bus lines on a profitable basis.

Yet, Keynesian central banking supposes 12 officials on the FOMC can read, assess and manage the endless myriad of complex information networks and financial variables that course through the nation’s multi-trillion currency, credit and capital markets, which are, in turn, are inextricably plugged into far larger flows of the same in the 24/7 global financial system.

Worse still, it has evolved that the small cadre of officials who now attempt statist administration of the most important prices in all of capitalism are wedded to a primitive Keynesian economic model that is hopelessly disconnected from the realities of the world’s highly integrated $80 trillion economy.

It supposes that the $20 trillion piece of that domiciled within the US national borders is an economic island unto itself. Or better still, a giant bathtub of GDP which needs to filled to the brim as quantified by the monetary politburo in the form of a guesstimate called “potential GDP”.

Moreover, this cadre of statist planners presume as axiomatic that capitalism on the free market suffers from the economic equivalent of ED. Left to its own devices, it never rises to the brim of potential GDP, and even has a tendency toward cyclical instability, recessionary decline and even worse (depression).

Of course, this presumption is the ultimate case of the cat calling the kettle black. The only real cause of economic setbacks that can’t be fixed by the free market itself are the financial and credit boom and busts caused by central banks themselves.

Thus, capitalism readily recoveries on its own from so-called “external shocks” caused by acts of god, such as droughts, floods and catastrophic storms. Even Cat 5 hurricanes do not cause local economies to spiral into an endless black hole; price arbitration causes outside resources to flow with aplomb into the economic vacuums wrought by mother nature.

The external shock of war—-especially total global wars like the two of the last century—-does unsettle the free market, but that’s because of wartime mobilization and control measures that distort prices and channel extraordinary amounts of economic resources into war and destruction.

But you don’t need central banks to solve that problem as demonstrated by the events of 1919-1921. The Great War ended, the machine of wartime control was dismantled wholesale, the vast diversion of capital and labor to war and destruction stopped and the central bank did nothing.

Within months of the Treaty of Versailles (July 1919), the free market had repaired the damage, righted the wartime mal-distribution of labor and capital, reversed the post-war recessionary impulses, and had sent American capitalism back into the booming growth trajectory that the Great War had interrupted.

In the Great Deformation, we addressed at length the recessions which occurred thereafter, including the Great Depression of the 1930s. Suffice it here to say that all 12 of them were not caused by the inherent infirmities of capitalism or failures of the free market.

To the contrary, they were the product of central bank instigated financial boom and bust cycles. That is, the unnatural and unnecessary product of state intervention, not the inherent tendencies of capitalism on the free market.

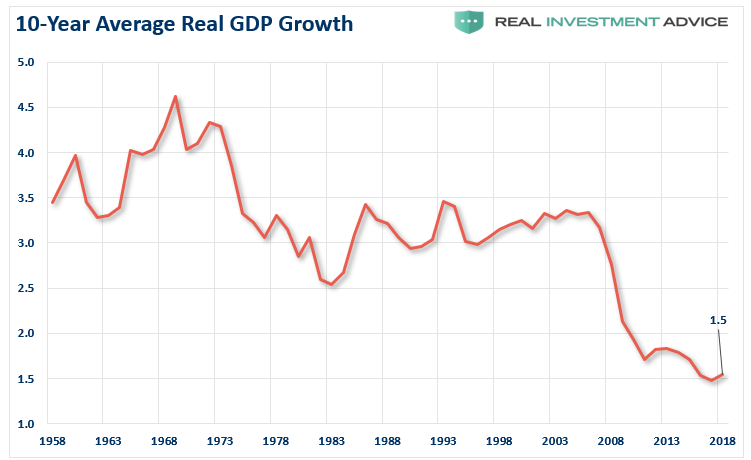

Likewise, the economic ED portion of the case can be readily refuted. The alleged Viagra of central bank stimulation and growth enhancement has been applied with increasingly heavy dosages ever since the 1950s and the results speak for themselves. The rolling 10-year rate of real economic growth has been trending southward in a nearly unbroken arc.

So in truth, there is no a priori case for the Economy mission of central banking at all. And besides, as a practical matter the very idea of targeting the inflation rate, the unemployment rate or any other broad macroeconomic variable in one country is just plain ludicrous and impossible.