Ironically, Donald Trump’s harsh, unhinged and unrelenting attacks on the Fed are about as good a warning sign of the impending Turbulent Twenties as any.

That is, if even the Donald can see that the Fed has morphed into an all powerful monetary politburo that threatens the very survival of capitalist prosperity in America, then the end of the 30-year financial fantasy launched by Alan Greenspan in October 1987 must truly be at hand.

The truth is, like no other politician since December 1913 when the Federal Reserve System was mid-wifed into existence by the great financial statesman, Congressman Carter Glass, Trump has exposed its awful secret.

Namely, that what Glass intended to be a modest, economically passive “bankers’ bank”, which would provide back-up liquidity to the banking system against good commercial collateral at a penalty spread above the free market rate of interest, has become an intrusive instrument of plenary monetary central planning by an unelected priesthood of delusionary central bankers.

The emphasis here is on the word “passive”. The kind of old-fashioned central banking on which the Fed was predicated in 1913 did not pretend to superintend the entire GDP or target the inflation rate or track the level of unemployment, housing starts, retail sales, CapEx orders, export volumes or anything else in today’s constellation of so-called “incoming data”.

Back then, most of these macro-economic aggregates had not yet been invented, let alone measured and tracked monthly and quarterly. And, in any event, the underlying level of main street economic activity and the growth rate of society’s wealth was understood, properly, to be the business of capitalism, not the state.

The macro-economic variables that today’s Keynesian central bankers obsess about, in fact, were way outside the remit of the Glassian Fed. The economic aggregates were taken as a given—the unwilled, unplanned, undirected outcome of millions of workers, entrepreneurs, investors, inventors, savers and speculators pursuing their own economic ends on the free market.

Accordingly, the Fed’s far more modest assignment was to provide market-priced liquidity and to foster financial stability within the four walls of the commercial banking system. That modest assignment, in turn, reflected the belief that market-based capitalism would take care of the rest.

Not surprisingly, therefore, the original central bankers were to be green-eyed shade accountants and commercial bankers. That is, experts capable of assessing bank balance sheets and the credit value of commercial collateral (real trade bills backed by finished inventory or sold goods) presented to the 12-regional Reserve Banks for discount loans, not PhD economists who pretended to comprehend and direct a continental economy.

Needless to say, between then and now, the 19 central bankers who comprise the Federal Reserve Board have given “mission creep” an altogether new definition. In fact, the Fed has morphed into a rogue agency endowed with open-ended state powers to dominate the entire financial system; and, by manipulating and falsifying the price of money, debt and most other financial assets, to thereby shape the ebb and flow of the nation’s entire $21 trillion economy.

So the Turbulent Twenties beckon for one reason above all others. To wit, the Fed’s regime of monetary central planning inherently causes failure on the main street economy and unspeakable windfalls to Wall Street and the wealthy elites who own most of the financial assets.

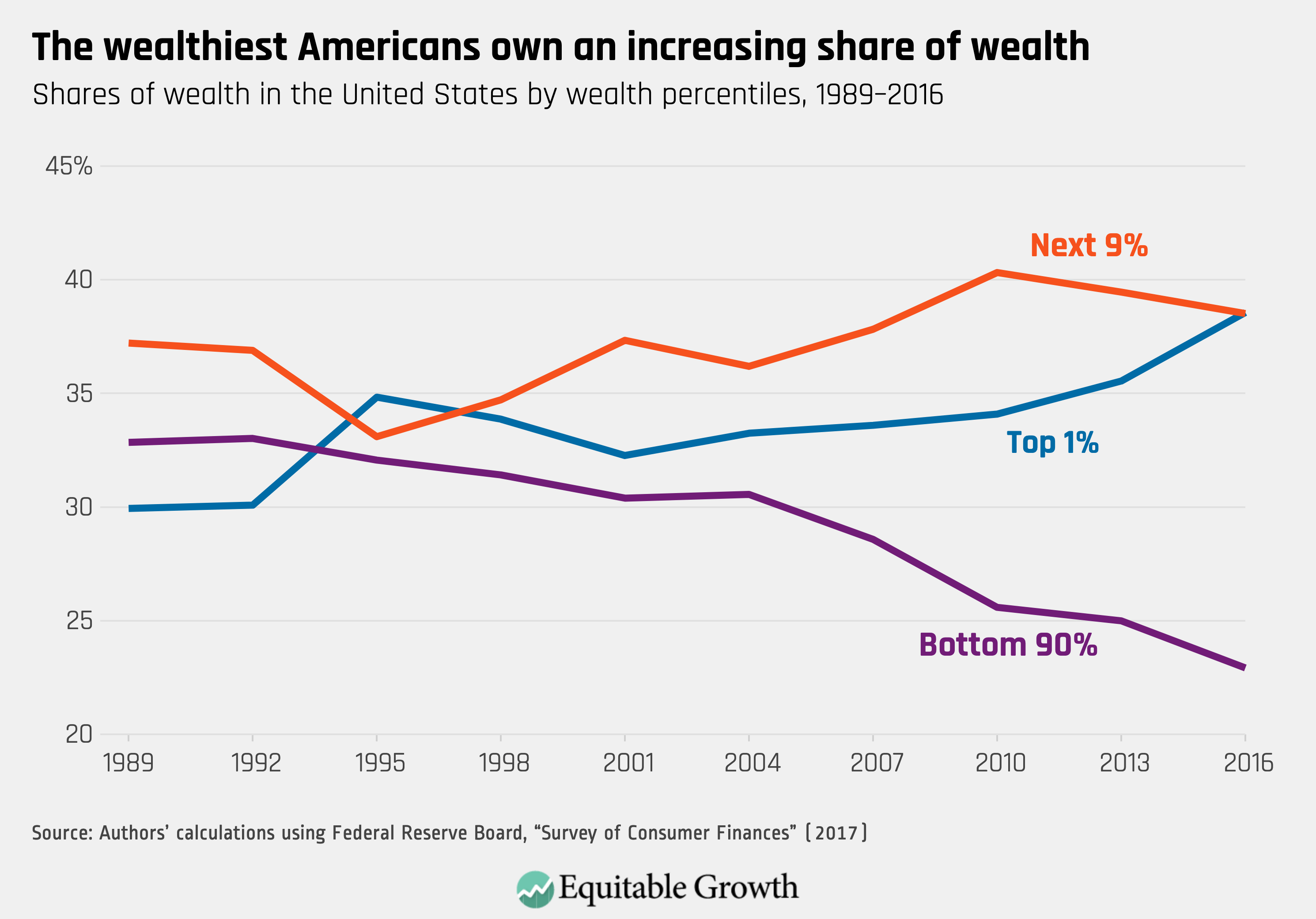

We will treat later with the reasons and mechanics by which Keynesian central banking causes a massive shift in financial wealth to the tippy-top of the economic ladder. But suffice it here to note that since 1989, the share of US net worth attributable to the bottom 90% of households (purple line) has dropped from 33% to 24%, while the share held by the top 1% has soared from 30% to nearly 39%.

Contrary, to Dem and liberal propaganda, however, this isn’t due to trickle-down tax policy. The low water market for tax rates was reached in 1986 when Ronald Reagan’s landmark tax reform bill cut the top rate for all forms of income—wages, salaries, dividends and capital gains—to 28%. Since then rates have risen steadily higher on earned income and have been only modestly reduced on capital gains.

Accordingly, the driver of the chart below is bad money, not pro-rich tax policies. As we will fully develop subsequently, the Fed’s massive balance sheet expansion since Greenspan took the helm—from $200 billion to $4.0 trillion or a 20X gain–is the culprit.

That’s because in today’s debt-saturated and globalized economy, Fed “stimulus” in the form of massive bond-buying and interest rate repression never leaves the canyons of Wall Street. It no longer causes credit-based growth spurts on main street—only relentless inflation of financial assets on Wall Street.

To be sure, the so-called Humphrey-Hawkins growth and inflation mandates are the cover story for this perverse regime. But in today’s fully integrated $85 trillion global economy these purportedly sacrosanct mandates amount to an unattainable, threadbare farce.

So the Donald’s everlasting service to whatever future prosperity may yet be attainable is this: Namely, the rambunctious calling-out in advance—and loudly and explicitly so—that the next financial crisis and resulting recessionary dislocation will be the sole responsibility of the Federal Reserve.

And that’s something totally new under the sun compared to the servile Fed-fawning exhibited by Obama, Clinton and the Bushes who came before.

At the end of the day, sound money scribblers and even the “End the Fed” candidacy of Congressman Ron Paul couldn’t break the spell—notwithstanding the truth of their case. They were and are marginalized by the mainstream financial press owing to the requisites of “access journalism” and the willful blindness of the corporate owners at the Wall Street Journal, Bloomberg, CNBC, Reuters and the rest.

But the Donald has a 60-million Twitter account, an audacious take-no-prisoners style of political modus operandi and a yawning empty space under the Orange Combover when it comes to even the rudiments of monetary policy.

But no matter. His crude political need to name and blame a scapegoat for the impending financial calamity—the Turbulent Twenties—is all that is required. That’s because his conclusion about the Fed’s culpability is absolutely correct, even if his hackneyed Easy Money reasoning comes from the deep bleachers in left field.

On Trump’s call for even lower interest rates and a resumption of QE, of course, he is totally wrong, but the Donald will bag his institutional prey nonetheless. That’s because unlike all of the other recent presidents—save for Ronald Reagan most of the time—who were totally choreographed, scripted, and moved their lips in the way that their advisors told them to on matters of monetary policy, the Donald is his own man when he hits the twitter keyboard.

Accordingly, the one thing that Donald Trump is going to accomplish in his misbegotten tenure is that his ferocious attack against the Federal Reserve will tear away the veil that it is a college of geniuses who are “beyond politics”; and that the Eccles Building and its 12 regional annexes are populated by high-minded technical experts in money wh0se essential work safeguards the prosperity of American capitalism.

To the contrary, the Donald’s escalating war on the Fed—-which is going to soon get far more vicious and heavy-handed—will tear apart limb-for-limb the arrogant pretensions of its 19-person monetary politburo, which has usurped control of financial and economic life in America, and, for that matter, on the fairest part of the planet.

Before the dust settles on the 2020 election, therefore, we believe that he will have totally besmirched and destroyed the credibility of the Fed, at least in the eyes of his base. At long last, there is going to be a popular-level political debate about central banking and what it actually accomplishes.

Needless to say, we relish the prospect. There is no way to get back to free market prosperity until our self-perpetuating cabal of Keynesian central bankers are politically lacerated and beaten to smithereens.

After the fragments end up all over the cutting room floor, we can figure out what to do next. But you must take down this institution first because the Fed is the #1, the #2 and the #3 enemy of prosperity, capitalism, free markets, individual liberty, and the wealth of people in America and in the world today.

Accordingly, the crucial starting point is debunking the Humphrey-Hawkins Act and the Fed’s so called full-employment and inflation mandates.

As to the latter, the Fed does not have a prayer of creating inflation, let alone hitting with precision its specious 2.00% inflation target. Suffice it here to say that in an integrated global economy driven by central banks engaged in a race to the interest rate bottom, the bias of the financial system is toward over-investment, malinvestment and deflationary over-production.

Here’s the smoking gun based on the Fed’s loudly ballyhooed contention that the only valid measure of inflation is the PCE deflator, and that the periodic shortfall from 2.00% of the latter since inflation targeting was officially adopted in January 2012 is the principle reason for keeping interest rates pinned far below market clearing levels.

The purple line represents a popular commodity index which is heavily influenced by global energy and other raw material price cycles. As it evident from the right-hand scale, the year-over-year global commodity index swung from negative 30% during the near global recession of 2015-2016 to positive 30% during the 2017-2018 China credit fueled mini-boom, and then back to zero percent or less in recent months.

During that same seven-year period, the PCE deflator swung from 2.5% (over-shooting the target) to just 0.5% per annum during the 2015-2016 global slowdown. It then sprang back to 2.3% during the mid-2018 sugar high and is now back to 1.5%, which, in turn, has generated calls for more Fed easing owing to an alleged inflation shortfall.

This is downright risible nonsense. The Fed interest rate machinations, stop and go maneuvers on QE/QT and open mouth operations had little to do with the fluctuations in the PCE deflator. They were due to global forces far more powerful than the Fed’s wet noodle policy maneuvers.

The implications of the chart below cannot be gainsaid. It completely debunks the very idea that the Fed is rationally pursuing higher inflation with its chronic policy of “accommodation”.

What is it “accommodating”, in fact, is the insatiable appetites for cheap money among its clientele on Wall Street.

Likewise, the global regime of Keynesian central banking inherently careens toward massive and cumulating over-indebtedness. That’s because at bottom there is no economic magic at all in its tired brand of borrow and spend “stimulus” enabled by cheap, falsified interest rates.

That policy panacea just pulls economic activity forward in time—at the cost of relentlessly accumulating debt and ever higher future preemption of income and cash flows for debt service. Yet once they are debt-entombed, economies are inexorably capable of ever more modest rates of growth.

That truth is written all over the subway walls, as Simon & Garfunkel once put it. Between 2001 and 2007, for example, global debt rose from $86 trillion to $140 trillion. At the same time, global nominal GDP increased from $33 trillion to $58 trillion during that six year period.

That is, $54 trillion or new debt bought $25 trillion of new GDP.

By contrast, debt exploded from the pre-crisis level of $140 trillion to $255 trillion by 2019, while GDP rose to just $85 trillion during the 11-year cycle subsequent to the pre-crisis peak.

That is, in the latest so-called recovery, it took $115 trillion of new debt to generate just $27 trillion of additional GDP. That’s $4 dollars of going into permanent hock for just $1 dollar of (temporary) current GDP.

Self-evidently, that debt-fueled route to nominal GDP growth has played out. The household sector is at Peak Debt. And the business sector has been lured into massive financial engineering, not productive investment, by the speculative casino on Wall Street, which is the end product of Keynesian central banking.

As we indicated above, all that massive central bank stimulus in the form of fiat credit expansion never escaped the canyons of Wall Street and its counterpart financial venues around the world. And there, it did cause growth and inflation, but of financial asset prices only, and egregiously so.

Accordingly, asset prices are now precariously purchased in the nosebleed section of history—-and not just stock prices, but bond prices, too. The $17 trillion of subzero yielding government and investment grade bonds in the world as of a few months ago are just hideously over-priced instruments of rank speculation.

But if you look at the charts, there are massive air pockets down below, let’s say, the 2700 level on the S&P 500.

If there’s a shock event—like some tankers blow up in the Persian Gulf, or something really bad happens in the Taiwan Straits, or the Chinese pull some real retaliatory stunt like dumping a couple ten billion of UST bonds in a few hours—it could ignite the sell-off fuse on a market which is overwhelmingly machine driven, thereby tanking the whole applecart.

After all, 80% of daily volume in the stock market is essentially either indexed driven ETF’s and mutual funds or various kinds of quantitative, machine-driven momentum-based investment strategies. If these carbon and silicon based chart-monkeys ever lose their numeric/formulaic footings, the market will drop through a deep air pocket, and then it’s all over except for the shouting.

That is, if the S&P 500 drops 400, 500 or 600 points, you will trigger another go around in the corporate C-suites. They’ll suddenly wake up, like they did in October 2008, and say, “Oh my God, we’ve got too much inventory, we’ve horded too much labor, we’ve got a lot of M&A assets that aren’t producing returns.”

And then the corporate C-suites will go into these big restructuring programs, where they layoff workers by the tens of thousands, and they take huge write-downs, close facilities and extinguish underperforming assets in order to appease the trading gods of Wall Street.

The next thing you know, of course, you have a C-suite triggered recession. That’s how it happens these days under the baleful regime of Keynesian central banking.

Recessions don’t happen anymore because the Fed is tightening credit costs on Main Street. That’s the old days. That’s your grandfather’s economy, and your grandfather’s Fed.

But we’re now in the era of Bubble Finance. The Fed basically inflates the financial system until it collapses, and then it spills over into the mainstream economy through these corporate C-suite panics.

So if the stock market cuts through the air pockets down below, the recession will happen instantly, and no one will see it coming—just like in 2008.

We remember well that in the spring of 2008 they were still talking about the Goldilocks economy. But in November 2008, they were talking about the end of the world.

This is exactly what we think will happen if the stock market breaks loose.

We don’t know when it will happen. It could happen before November 2020, or after it. No one can really predict.

But we think the odds are that it will happen before the election, and if it does, the Donald is toast.

Under that scenario, Elizabeth Warren will be the next President of the United States, and as that prospect becomes ever more probable, the panic in the stock market will be something to behold. It will be worse than anything we’ve seen since October 1987.

Indeed, if the stock market is faltering in November 2020, or it has actually crashed, and the economy’s in trouble, you’ll have a populist, redistributionist, big government, statist President and Congress.

That’s a totally different world than the fantasy that we’ve been living for the last 30 years.

And that’s what’s going to make the Turbulent Twenties an altogether different ball game.