B-Dud (aka William Dudley), former President of the powerful New York Fed and designated Goldman plenipotentiary to the nation’s ruling monetary politburo, just let a giant cat out of the bag.

That is, by properly warning that the Fed should not be enabling and rewarding the Donald’s lunatic Trade Wars via easing moves designed to offset the damage, he actually raised a far larger question which cuts right to the quick of the Fed’s raison d’ etre.

To wit, if the Fed’s self-defined mission is to improve the performance of the macroeconomy compared to what would otherwise be its un-chaperoned path, then what happens when that sub-optimum (i.e. recessionary) path is caused by counter-productive, avoidable or even stupid actions by agencies of the state?

The Donald’s blunderbuss Trade War is a pretty obvious case of policy stupidity, which threatens growth, jobs and incomes.

And the former monetary central planner makes his stance on the matter quite clear: By attempting to mitigate the economic damage, the Fed would actually be enabling and perhaps encouraging an escalation of the Donald’s attack on global supply chains and domestic importers and consumers:

U.S. President Donald Trump’s trade war with China keeps undermining the confidence of businesses and consumers, worsening the economic outlook. This manufactured disaster-in-the-making presents the Federal Reserve with a dilemma: Should it mitigate the damage by providing offsetting stimulus, or refuse to play along?

But what if the Fed’s accommodation encourages the president to escalate the trade war further, increasing the risk of a recession? The central bank’s efforts to cushion the blow might not be merely ineffectual. They might actually make things worse.

The answer is damn obvious if you take the boundary case.

We are here referring to the day that the Donald wakes up totally disturbed by another taunt from the Chinese or is baited by some ultra-China hawk on Fox & Friends, and proceeds—orange combover akimbo—to announce that US ports are “hereby ordered” to refuse all cargo originating from China.

If the Fed were to “ease” print money in the face of that kind of insanity, of course, the jig would be up. It would be obvious that the Eccles Building is run by a ship-of-fools who have a purely Pavlovian reaction function: That is, they will bang the Easy Button on any and every anti-growth provocation—no matter how dangerous or absurd its origin.

Indeed, in taking B-Dud to task for essentially blurting out that the Emperor has no clothes, some knucklehead Wall Street economist made exactly that pavlovian case.

Said he in so many words, the Fed is Wall Street’s financial bitch—so in the face of anything which smacks of “lower growth”, which is code for lower stock prices, it needs to get Easy and then still Easier.

“Bill Dudley’s remarks are not only misguided but also dangerous coming from a former top Fed official,” said Gregory Daco, chief U.S. economist at Oxford Economics. “The Fed doesn’t have the luxury to stand idle in the face of a slowing economy.”

Really?

The implication is that mitigation and counteraction are open-ended missions, and that, implicitly, the Fed’s job is to scurry along behind the government horse parade with shovel, broom and cart scooping up whatever smelly deposit is put in its path.

But does that injunction encompass say, a President Elizabeth Warren’s harsh wealth tax on the 0.01% which causes the stock indices to plunge?

Even the Wall Street guy who got it right inadvertently pointed to the real problem:

Dudley “is dead right” that the Fed shouldn’t cushion trade impacts, said Roberto Perli, a partner at Cornerstone Macro LLC. “The risks to the outlook that are quite evident right now have nothing to do with interest rates being too high and a lot to do with trade tensions and unprecedented policy randomness depressing household and business confidence.”

Right. The real problem with the Donald’s growth-retarding Trade War is not too high interest rates. But in fact, that truism pertains far beyond the growth barriers posed by tariffs run amuck.

The real problem facing the American economy at this late stage of the business cycle is that there is hardly any semblance of interest rates left at all, and that clearly is the doing of the Fed itself.

Earlier today, the 10-year UST yield touched 1.46%. So we don’t care what long or short inflation ruler you use, the benchmark security of the entire US financial system—and of the global markets, as well—is trading at a deeply negative real yield.

In the case of the CPI less food and energy, for example, the year-over-year inflation rate has exceeded the Fed’s magic 2.00% target for 17 months running, and for the 12 months ending in July the rate of increase was 2.21%.

Accordingly, a fair approximation of today’s real yield on the 10-year UST is negative 75 basis points.

In the face of that reality, of course, it borders on the surreal to hear the head of Black Rock’s $2 trillion AUM in fixed income markets, Rick Rieder, demand on bubblevision that the Fed cut rates by 50 basis points at the September meeting because the US economy is in need of “more accommodation”.

Stated differently, if a real 10-year rate of -0.75% is more than the US economy can bear there is something fundamentally rotten in Denmark, and it ain’t Greenland!

The point here is that the Fed and its fellow-traveling central banks have essentially disabled the navigation and signaling system of global financial markets. With $17 trillion of negative yielding sovereign and investment grade debt in the world, and the entire yield curve at or near subzero levels in Europe and Japan, desperate yield- seeking money is now flowing into the US dollar markets as the last port in the storm.

SUBSCRIBE TO CONTINUE READING

Already a subscriber?

Login below!But a 50 basis point cut in the totally administered and artificial Federal funds market will not stem the flow of hot international capital; it will actually accelerate the race to the bottom of the interest rate market until there is no positive yield left anywhere on the planet.

That’s because after 30 years of money-pumping by the central banks, honest price discovery is dead. The casino is now just a herd of stampeding financial caribou chasing whatever security is going up. So another big rate cut will be taken as a siren call that more Fed easing in the form of the only tool it has left—-bond buying or QE—is just around the corner.

But QE is a financial cancer. It powerfully encourages leveraged front-running by speculators who have learned over and again during the last decade that it pays—bigly—to buy what the Fed (and other central banks)will be buying because the price of such securities inexorably rises.

In turn, a continued plunge lower of the 10-year UST yield (and rising price) will only suck in more yield-hungry foreign capital in search of not just positive yield, but short-run speculative gain. That is, the central banks have turned the fixed income markets upside-down—-with price appreciation rather than safety of principal and certainty of modest yield now completely in the driver’s seat.

Indeed, just a review of the 10-year yield path during the past 10-months underscores the interest rate death spiral now underway in the last sovereign debt market with a positive integer in front of the yield. To wit, on November 8 last fall, the yield stood at 3.26%, meaning that yields have collapsed—and prices soared—by 180 basis points are by 55% since then.

With this kind of massive price momentum already underway, an aggressive Fed easing campaign like Wall Street and the Bully Boy in the Oval Office are now clamoring for would likely turn the US Treasury market into the equivalent of a financial black hole: The descent of yields toward zero would be quick and violent as unhinged speculators and front-runners piled on for the ride.

Needless to say, a world without interest rates would not foster improved performance and growth on main street for the reason cited above: Namely, the cost of capital is not, and has not been, a barrier to either business investment or consumer spending.

In the case of the former, even the $400 billion business tax cuts being accrued in 2018 and 2019 owing to the Trumpian/GOP tax cut have stimulated no sustainable CapEx pick-up whatsoever. In fact, as shown in the chart below, the initial sugar high is already all over save for the shouting.

From an initial 8% real growth rate in early 2018, the quarterly annualized rate of business fixed investment growth has actually plunged into negative territory, posting at a -0.7% rate of decline in Q2 2019.

The chart below not only reminds that interest rates have nothing to do with the faltering pace of the main street economy, but also the absolute intellectual corruption that has polluted the Wall Street narrative.

The aforementioned Black Rock fixed income head knows full well the implications of the chart below. But he was happy to appear on bubblevision anyway to talk his book and lure whatever Greater Fools which remain in the casino into a runaway bond market that is heading for a massive implosion.

Even more importantly, the chart above reminds about the true impact of Keynesian central banking. It is an absolute growth killer on main street because it generates massive malinvestment and speculation, which diverts corporate America’s cash flows and balance sheet capacities from the productive investment in the main street economy to full throttle financial engineering.

In the healthy free market economy of yore, in fact, corporations came to Wall Street to sell stock, and then cycle the proceeds into new capacities, new efficiencies, new output and new jobs.

By contrast, under the Bubble Finance regime of Keynesian central banking, companies come to Wall Street to buy their own stock, and massively so, thereby disgorging the economic surpluses generated by the working masses to the brokerage accounts of the top of the ladder economic classes who own 85% of the stock.

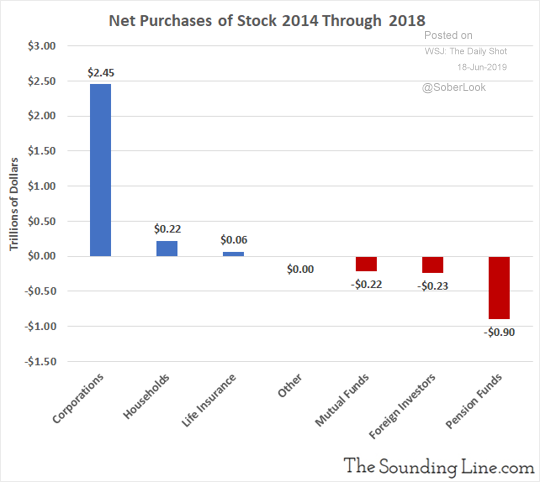

As shown below, corporate share buybacks currently account for roughly all ‘net purchases’ of U.S. equities in recent years. And that’s a massive economic debit to healthy investment and long-term growth.

Moreover, the perverse effect of drastically mispriced debt capital and central bank-induced speculative mania on Wall Street has been to essentially strip-mine the middle class.

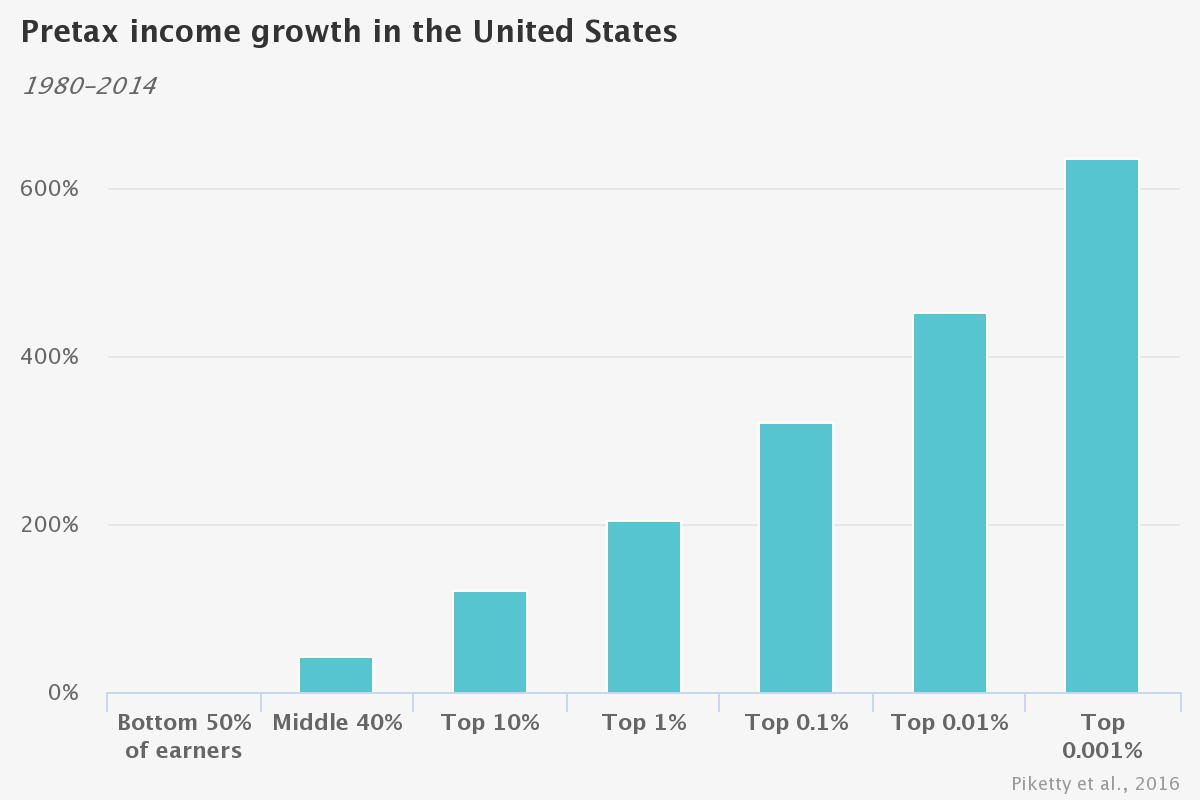

That is, income growth has overwhelmingly been concentrated at the top of the economic ladder as the US industrial economy has been off-shored to China and other low labor cost venues by the Fed’s idiotic 2.00% inflation target for the domestic economy. As Lance Roberts cogently noted in today’s post:

The top 1 percent of US adults now earns on average 81 times more than the bottom 50 percent of adults; in 1981, they earned 27 times what the lower half earned.

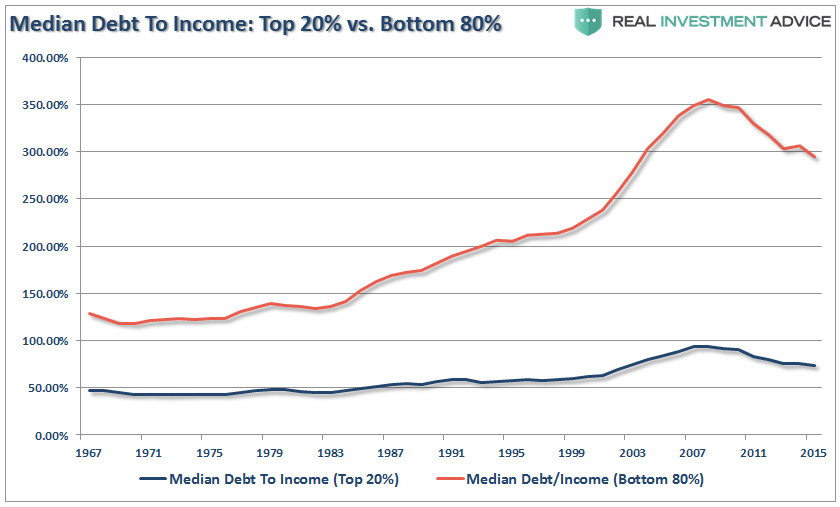

As Roberts further noted, it should not be surprising that personal consumption expenditures, which make up roughly 70% of the economic equation, have had to be supported by surging debt levels to offset the lack wage growth in the bottom 80% of the economy:

There is a vast difference between the level of indebtedness (per household) for those in the bottom 80%, versus those in the top 20%.

What this means, of course, is that 80% of US households are still tapped-out—stranded at Peak Debt with leverage ratios nearly triple the healthy and sustainable levels that prevailed during the heyday of US growth and middle class prosperity prior to the arrival of Alan Greenspan at the Fed in 1987.

In short, Fed policy is now thoroughly anti-growth. It can’t stimulate incremental borrowing and consumption among the bottom 80% of households because they are stranded at Peak Debt.

And it actually encourages the business sector to liquidate capital and cycle it back into the Wall Street speculative arena.

So, yes, the Fed should not “accommodate” the Donald’s Trade War madness.

Better still, it should stop accommodating its own far more damaging assault on capitalist prosperity.

Stated differently, free market capitalism doesn’t have any growth deficit or irreversible cyclical instability. Workers, businesses, savers, investors, innovators, inventors and honest speculators on the free market all aspire to improve their economic circumstances and wealth, and thereby relentlessly and assuredly propel the aggregate economy forward along an un-chaperoned path of growth.

Capitalism doesn’t need any stinkin’ help from the state and its central banking branch. In fact, like the Donald’s Trade War roadblocks, it is the state and the state alone that introduces obstacles to growth and cyclical instability—including every recession since WWII and the Great Depression which proceeded the latter.

So after all these years dwelling in the inner sanctum of the central banking beast, B-Dud is actually on to something, albeit surely unintended.

To wit, central bankers should not only abjure attempts to heal the economic wounds caused by other branches of the state; they need to stop administering the far greater wounds to main street prosperity that are the inherent result of Keynesian-style monetary central planning.

[Continue reading]: