Festering in the 10-year shadow of the Lehman event, the Wall Street narrative has never been so dumbed-down and heedless as it is today. For example, MarketWatch sounded the all-clear to the dip-buyers this AM by describing today’s CPI release as an “underwhelming inflation report”.

Apparently, this was warranted by a minor swiggle in the year-over-year sequence of the index, which caused July’s 2.9% gain to slip to 2.7% in August. For our money, of course, CPI inflation at virtually the same rate as the 2.8% year-over-year gain in wage rates does not bespeak of Goldilocks or even an economy glowing faintly pink of health.

Instead, it is a reminder that living standards for Flyover America are dead-in-the-water and have been for most of this century; and it also implies that 10 years of today’s “underwhelming” inflation rate would reduce the value of a household’s hard-earned savings by 25%!

SUBSCRIBE TO CONTINUE READING

Already a subscriber?

Login below!Besides that, there really wasn’t anything underwhelming or better about the August CPI at all. The annualized rate of change during the month was 2.67% and that was actually up considerably from July’s reading of 2.05%.

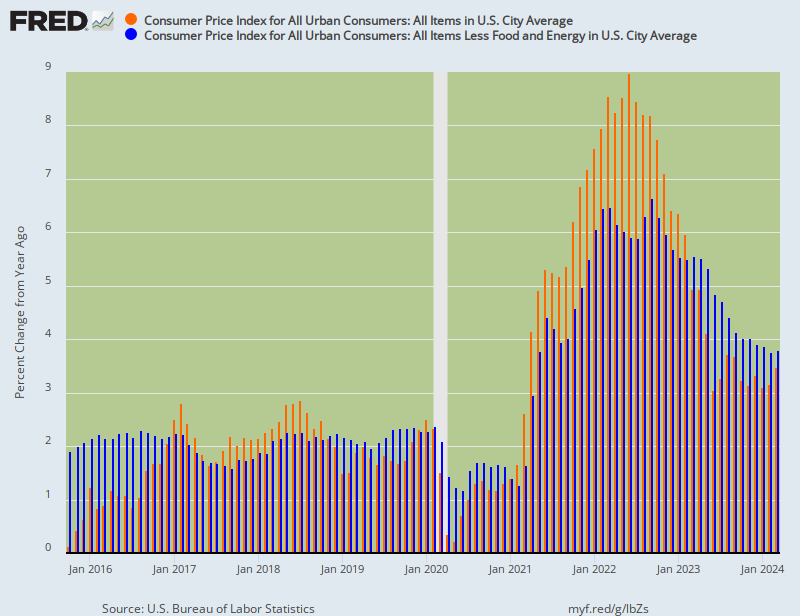

Indeed, here is the cost of living picture with and without food and energy for the last 35 months. We don’t see anything reassuring about the inflation trend at all.

On a year-over-year basis, the headline CPI (orange bars) has been above 2.7% for the last four months running, and even the so-called core rate (blue bars) has been above the allegedly magic 2.00% marker for 23 of the last 35 months.

Our point, however, is not to quibble about the most recent inflation rate squiggles. Rather, it is to remind that all of today’s celebratory rhetoric about how the allegedly “courageous” bailouts and money-pumping spree 10 years ago have succeeded splendidly and restored a booming economy are just self-serving bunkum. And exceedingly dangerous poppycock at that.

To be sure, Wall Street claims a roaring success because it’s peddling stock to the sheeples. And the Fed keeps taking full-employment victory laps because there is nothing better than a Big Lie to justify its massive usurpation of power in the financial system, where it has essentially ash-canned honest free markets and price discovery.

And most of all the Washington politicians—including the madman un-politician now in the Oval Office–embrace the “it’s all fixed and better than ever” narrative because it obfuscates the monumental fiscal trap into which they are leading the country.

On the latter score, the complete yawn in Washington on the recent announcement that the Federal government borrowed the whopping sum of $214 billion in the month of August proves the point. This was not only one of the highest monthly deficits on record, but also the highest August deficit ever.

Moreover, that number was no aberration, but indicative of a trend that is absolutely perilous.

To wit, the net public debt on Tuesday stood at $21.2 trillion compared to $20.0 trillion at the equivalent point a year ago. That means Uncle Sam has borrowed in the last 365 days alone about $1.2 trillion or 6.0% of GDP in what is now the tenth year of a business expansion.

Indeed, the rolling 12-month deficit trend displayed in the chart below is far, far more important than the aberrant Q2 real GDP growth rate of 4.2%, which is already slouching back toward 2.0% based on the data for Q3 already available.

The truth is, there has never been a doubling of the deficit run rate this late in the cycle. In the face of the Fed’s belated shift to QT, in fact, it is a veritable invitation to a bond market crunch that nary a soul on either end of the Acela Corridor has even noticed.

Needless to say, there have been only two business cycles since WW II that even made it to their tenth year. And in the most recent one, covering 1991-2001, the Federal government was actually running a 2.3% of GDP surplus during year #10.

Likewise, during the long expansion cycle of 1961-1970, the final year deficit came in at only 0.3% of GDP. And even during the more abbreviated 72 month expansion cycle preceding the Great Recession, the 2007 deficit was just 1.1% of GDP.

Still, our point is not merely that Washington’s is insouciantly trifling with an unprecedented late cycle borrowing spree; it’s that Washington is flat-out defying the ineluctable math embedded in the present trends.

That is to say, during the last 11 years—on a cycle peak-to-peak basis, which is the only honest way to assess fundamental trends—-nominal GDP growth has averaged just 3.2% per annum.

So all except the most arithmetically challenged Congress people should be able to grasp the baleful equation at hand. That is, if GDP is growing at 3.2% per annum and you are borrowing 6% of GDP each year—then the upkeep on your debt service will eventually become the downfall of your solvency.

And there is virtually no escaping the math over any reasonable period of time. For instance, during the last 11 years there actually occurred one of those pesky (and predictable) things called recession, which inherently dent the average growth rate owing to the resulting stretch of negative real GDP and diminished inflation.

The 19-month swoon known as the Great Recession, in fact, generated an average nominal GDP growth rate of negative 1.7% per year. When combined with the 4.0% per year growth rate during the 36 quarters of recovery since then, the average nominal GDP growth rate between Q4 2007 and Q2 2018 computes to just 3.2% per annum.

In the interim, of course, the rate of government debt accumulation accelerated sharply during the worst of the downturn.

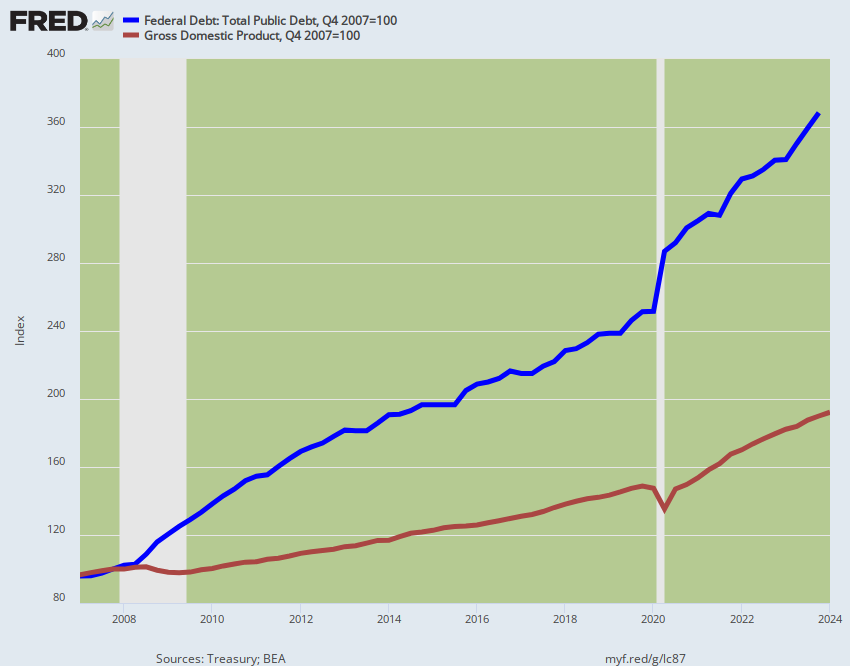

During the most recent economic cycle, therefore, the pubic debt (blue line) grew by 130% or 8.3% per annum, and that was nearly 2.6X the 39% gain in nominal GDP (red line).

And that’s where you get to the dead end of all of those “deficits don’t matter” assurances. There is simply no reason to believe that the last decade’s trend rate of nominal GDP growth (3.2%) is going to accelerate meaningfully; and under an inflation-indexed tax system, it is nominal GDP, not real GDP, which drives revenue collections and the deficit.

In theory, of course, you could sharply curtail the built-in rate of Federal spending growth; or, in the alternative, assume that the business cycle has been permanently repealed and that there will never be another recession. Well, at least through the current 10-year budget horizon to 2028, which would mark 230 straight months of business expansion or nearly 4X the average recovery cycle and 2X the record expansion.

Needless to say, the odds of either outcome are somewhere to the far side of that sliver of daylight between slim and none.

On the spending matter there is now no known political party in the US which wants to cut the budget. Period.

Trump is a borrow and spend Keynesian; the GOP middle-of-the-roaders would never touch the massive retirement and medical entitlements, even if the Donald took a powder on the matter, which he won’t; and the right-wing Freedom Caucus is mostly comprised of defense hawks and big spenders on the Pentagon side of the Potomac.

For the lack of doubt, just consider the chart below on the accelerating rate of Federal spending.

The most striking number in today’s Treasury report on last month’s budget trends was that August outlays soared to $433.3 billion—a figure which was not only 30% higher than a year ago, but the highest government monthly outlay of any month on record (and only slightly exaggerated by a timing issue).

When you consider the big items in that humongous August spending total, it doesn’t take to0 much imagination to see that the nation’s fiscal freight train is heading for the wall: Social Security outlays totaled $108 billion, with defense at $65 billion, Medicare at $83 billion and interest on the debt at $32 billion.

Obviously, there is not a corporals’ guard on Capitol Hill interested in cutting the first three items, but it’s the last of the Big Four which highlights the real trouble ahead.

You’ve got to pay the interest, and after the false holiday of the last decade owing to the radical interest rate repression by the Fed and other central banks, debt service is already beginning to soar.

It hit an all-time high of a $538 billion annualized run rate in Q2 2018, and in short order to will be rounding the trillion per year mark and heading ever higher.

At the same time, there is no prospect whatsoever of 10 more unbroken years of expansion as currently assumed by CBO and Wall Street economists. At least not when the Fed, the ECB and soon most of the other central banks of the world are pivoting to QT (quantitative tightening).

Stated differently, the implicit assumption on both ends of the Acela Corridor that recessions have been banished forever ain’t about to come true in this world—or likely even the next.

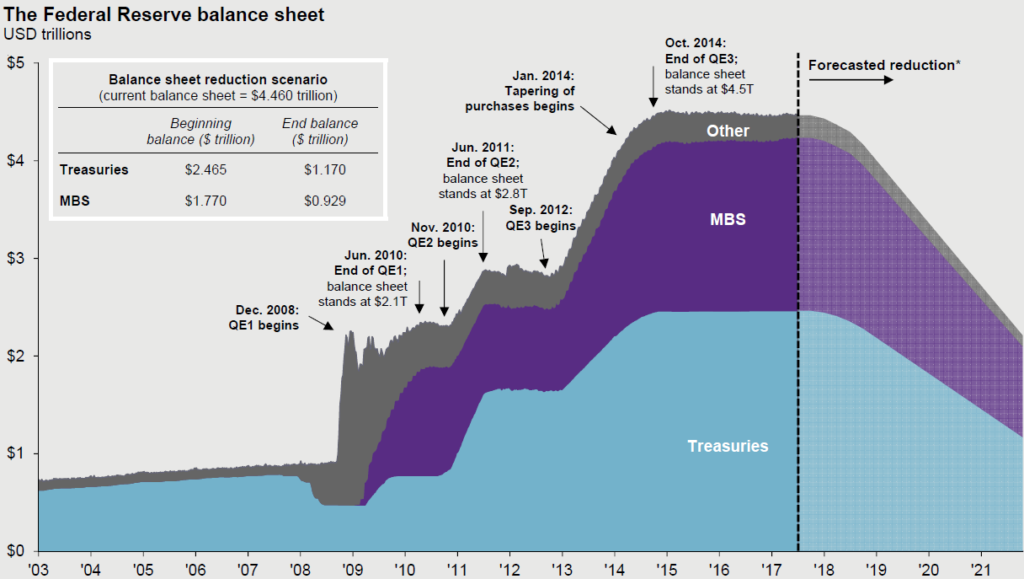

That’s where the concept of unprecedented monetary headwinds comes in. In fact, the only reason that 130% growth of public debt over the last years did not crush an economy which expanded by only 39% is lurking front and center in the chart below.

To wit, during the same period the Fed’s balance sheet exploded by nearly 500%, thereby permitting upwards of $3.7 trillion of the new public debt to be monetized by the Eccles Building money printers—plus trillions more by their fellow traveling central banks around the world.

Needless to say, the central bank pivot to Q2 is 100 times more important than then seasonally maladjusted quesstimates for the last 30 days of jobs and CPI and 90 days of GDP which dominate the mainstream narrative.

That’s because the one and only reason that the US economy has been able to stumble along on even the +/-2.0% growth track of the past five years is that the central banks were fraudulently clearing the bond pits of debt paper at rates dramatically below market clearing levels.

No more. The rising wall of the Fed’s debt monetization reached its peak back in October 2014 and for no reason except the palpable fear in the Eccles Building of a Wall Street hissy fit, it remained plateaued there for three years.

But now the March downhill has begun in earnest, and within three weeks the run rate of shrinkage will hit a $600 billion annual pace. Moreover, the self-congratulating Keynesians who run the Fed are as bamboozled by the deceptively glowing picture of the US economy in the rearview mirror as are the typical day-trading denizens of the casino.

So Jay Powell & Co are not about to abandon their QT path any time soon. Nor have the bond pits been exempted from the law of supply and demand.

Accordingly, during the next several years the “demand” side is going to be lightened by upwards of $2 trillion as the Fed de-monetizes the debt it accumulated during the post-Lehman money-pumping spree.

The central bank coddled speculators on Wall Street and clueless spenders in the Imperial City seem to think the vast cash drain depicted below will happen like a tree falling in an empty forest.

No one will purportedly notice!

Not so. When bond prices get real, the canyons of Wall Street will resound with financial thunder, and not of the good kind.

Nor is this purely a homegrown problem. During the initial crisis of 2008-09 and during several intervals since then, the major central banks of the world have expanded their balance sheets to the tune of 3-4% of GDP annually.

The truth of the matter is that amounted to the greatest planet-wide financial fraud in recorded history. The central banks were essentially printing new spending power from thin air at a rate faster than their average growth of GDP (the chart excludes China and the EM).

Yet that’s precisely why the present inflection point is so crucial. The Fed is already in the balance sheet shrinkage business, and even the mad money-printer, Mario Draghi, announced this morning that the ECB printing presses will go quiet on the last day of 2018.

So next year the only money printer left will be the BOJ—and even it is slithering around in search of ways to tamp down its rate of accumulation–lest it end up owning 100% of Japan’s mo9numental public debt and a fair share of public equities and ETFs, too.

In short, the relevant narrative is the one in the graph below—-that’s what in the windshield dead ahead.

But as the man on late night TV says, but wait. It’s worse.

At 10:15 AM this morning–less than 2 hours after the so-called “underwhelming” CPI print, the Donald essentially said: Not so fast!

The Wall Street Journal has it wrong, we are under no pressure to make a deal with China, they are under pressure to make a deal with us. Our markets are surging, theirs are collapsing. We will soon be taking in Billions in Tariffs & making products at home. If we meet, we meet?

Rarely have more ignorant words been issued from the Oval Office (or East Wing residence, as the case may be).

That is, no one has called off the Trade War—just because the hapless Mr. Mnuchin at Treasury attempted an end-run via a leak yesterday afternoon to the Wall Street Journal about another alleged initiative to talk nice with the Red Suzerains of Beijing.

But when it comes to Trade, the Donald’s doesn’t talk nice and won’t act that way either—-not until they finally put him on the Dick Nixon Memorial Helicopter for his final ride the Gonesville.

In the interim, tariffs will be rising, the CPI will be gaining, the public debt will be soaring and the rearview mirror will be glowing—-but with the belated bonfires of a Great Bailout that only paved the way for worse.